Year 2020 hasn't been exactly all bright and blooming for most of us. With COVID-19 around us, one cannot deny the impact that COVID-19 have brought upon us. Some have lost their job, some had to close down their businesses due to the lack of revenue, and some were forced to take unpaid leave or pay cuts.

Whilst the government have came up with several economic stimulus packages, one may also argue that it is insufficient especially for those struggling to meet ends' need. With that, EPF have been mostly been put on a spotlight recently on whether to allow members to dip into their retirement savings to meet ends need (today) vs. safeguarding their retirement future (tomorrow).

We have seen discussions all over the place - from high profile politician's comment, public's opinion, to the extend of EPF CEO's public comments with the Ministry of Finance, or even debates in parliament.

What does it really mean to all of us as individual contributors with all the withdrawal facilities (i-Sinar, i-Lestari) or investment facility (i-Invest) or reduced mandatory contribution rate from 11% to 9% throughout 2021? There has been many debates on these topic, even amongst the contributors. Some firmly believes in staying the course and swear NOT to touch EPF being their investment nest; whereas some will tap into any opportunity provided by EPF to withdraw their funds for specific purposes.

I have summarised some of my personal thoughts on these topics but before we get there, let's first establish some basic understanding on EPF!

Also known as the Employees Provident Fund (EPF), which basically is a provident fund (a.k.a. retirement fund) established back in 1951 to help Malaysian workforce to save for their retirement in accordance to the Employees Provident Fund Act 1991.

Just like most of the provident/retirement fund in the world, it is a forced-savings approach with contributions from both Employees & Employers (or voluntary self-contribution for those whom run their own businesses) as an attempt to ensure that its citizen would have sizeable funds during their retirement years.

According to a recent study conducted by AKPK, majority of us Malaysians are not prepared financially for our retirement years and that's a bad sign for us. Many may not even be aware to the fact that they will need "larger amount" of retirement funds to sustain the "current lifestyle" they have during their retirement years, thanks to the inflation.

For example, if we're spending RM1000 a month today, we will need approximately RM1350 a month to afford the same lifestyle 30 years later, assuming 1% annual inflation rate. I myself, for one, will definitely not be able to survive and retire with just RM1000/month; let alone with the living expenses post-inflation.

Unfortunately, not much information is available on EPF's investment aside from the supposedly annually published reports. You can find KWSP Publications here for reports up to 2018, and somehow they "hid" the 2019 Annual Report here. Took me a while to realise that... I have been wondering what happened to the 2019's edition with 2020's already coming to an end while preparing for this article.

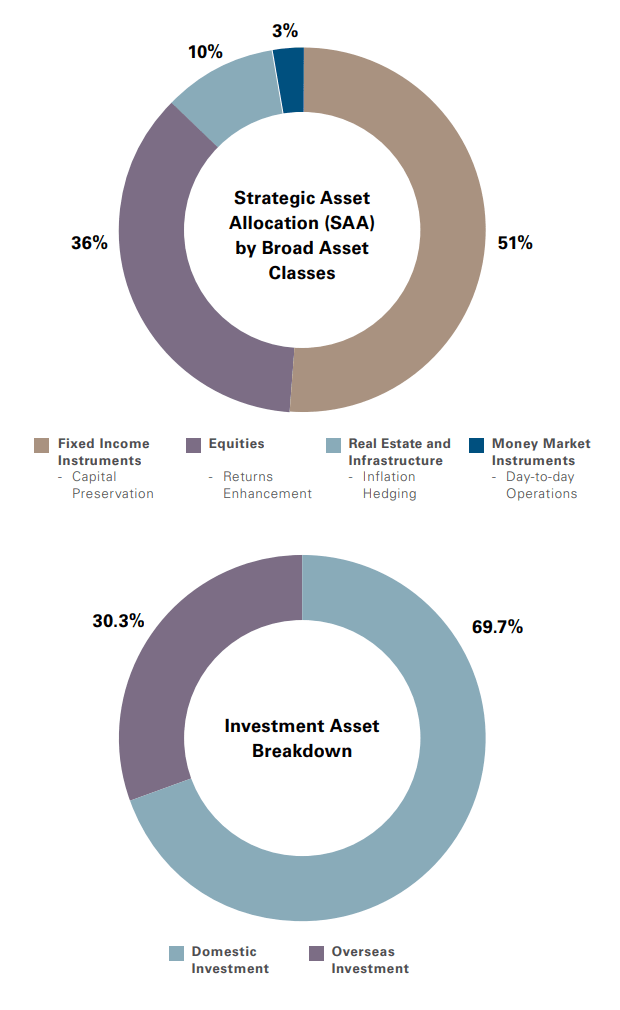

EPF's investment decision are mainly guided by their Strategic Asset Allocation (SAA) framework which focuses on optimising EPF’s long term investment return within the tolerable risk limits. The portfolio are primarily built up by fixed income instruments focusing on capital preservation and equities focusing on enhancing returns.

To put things into perspective, as of end 2018, EPF manages a total investment asset of RM833.76 billion (source: 2018 annual report) and the fund size have grown to RM924.75 billion by end of 2019 (source: 2019 annual report) after factoring in deposits and profits.

Based on 2019's data, they have invested RM360.44 billion into equities. By using the 69.7% domestic investments as a benchmark, we can safely assume that at least RM251.23 billion are invested into local equity market. This itself is is close to 15% of the entire Market Capitalisation in Malaysia, which was reported to be RM1,711.84 billion by end of 2019 (source: Securities Commission Malaysia).

Despite that overseas investment only accounted for 30.3% of their investment assets, it have however contributed 41.0% of gross investment income. In terms of the Return on Investments (ROI) in 2019, foreign investment attributed to 7.78% while the domestic investment attributed to 4.90%.

In a way, as the fish (EPF) is growing bigger and bigger as year passes by, the pond size (Malaysia Market) remains mostly stagnant. If we just take a look at the top 30 holdings by EPF today, you'll already see that EPF already owns significant portion for most (if not all) major local companies.

Without the freedom being given to EPF to further diversify into international markets, they will be stuck with more than 70% invested locally which may potentially hamper their upsides for long-term growths.

As part of EPF's initiative to empower the members to take charge of their own financial future, starting from their own unit trust investments. EPF have released i-Invest since August 2019 enabling eligible members to make informed decisions and manage their own unit trust investments.

With i-Invest, sales charge are capped between 0% to 0.5% which are way below the industry's average of 3% to 6% (or Fundsupermart Malaysia's 1% to 2%). In the past, if one were to diversify into Unit Trust Funds using their EPF Savings, they have to go through agents, fill up a tons of forms, and get charged with typical unit trust Sales Charge depending on platform. EPF's i-Invest eliminated most of these barriers by going digital and enforcing a cap to the maximum sales charge at only 0.5%.

Since its' launch on August 2019, members have been tapping into the opportunity by managing their own unit trust portfolios offered by various Fund Management Institutions (FMIs). The total transaction value have grown close to 7 times as of April 2020, with total transacted value of RM219.3 million from the initial RM32 million on August 2019.

Effective 1 May 2020, EPF have also waived all sales charge imposed by FMIs for investments transacted through i-Invest via EPF i-Akaun, for a period of 12 months ending 30 April 2021. This provides opportunity for members to diversify their EPF portfolio with zero upfront cost, though annual fund management fees will still apply.

As with before, there are certain eligibility to be met in order to diversify your investments into approved funds:

You might be curious on the definition for "sufficient savings". Basically, EPF have defined an ideal minimum target savings based on members' current age, to ensure that they will have enough saved when they hit 55 years old. You can check out the "minimum basic savings" table in EPF's website here.

Based on the "minimum basic savings", 30% of the excessive amount in Account 1 can then be invested into your fund choices via i-Invest facility, with minimum starting from RM1,000.

Invest-able Amount = 30% * (Balance in Account 1 - Minimum Basic Savings)

If you met the eligibility criteria and also have at least RM1,000 as investable sums, the next common question would be the following.

In the end it really depends on your personal circumstances, risk appetite, investment horizon, and pre-existing portfolio. I asked myself this question recently and debated whether if I should diversify my investments by leveraging the 0% sales charge provided by EPF i-Invest.

Ask these questions to yourself:

Some of the most common mistakes I have seen are those whom have been switching funds on a very high frequency - as if they are "trading" unit trusts as stocks. Investing should always be a long term game (>5 years) and one should avoid timing the market, but rather focuses on time in the market

Personally, after assessing my own situation, I have decided to further diversify my portfolio using the funds I have in EPF into several high-risk regional/global equity funds, as my current portfolio is overly exposed (>55%) to Malaysia market (mostly thanks to the heavy domestic allocation by EPF). Additionally I also have a rather long investment horizon (at least 3 decades) for me to go through various cycles of market up and downs.

In a nutshell, i-Lestari and i-Sinar was developed as an initiative to provide relief to members whom were negatively affected financially due to COVID-19 and the economy.

i-Lestari allows member to withdraw RM500 from their Account 2 on a monthly basis, effective 1 April 2020, providing up to 12 months withdrawal or end of validity period on March 2021, whichever is earlier. (source: i-Lestari FAQ)

i-Sinar allows member to withdraw an one-off advances between RM4000 - RM9000 or higher from their Account 1 (depending on your available balance). The advances must be replenished in which all future contributions will be allocated 100% to Account 1 until such time where the withdrawn advances are fully replenished. (source: i-Sinar Press Release)

As most Malaysians already do not have sufficient savings for their retirement, these should typically be rendered as the last-straw when no other better options are available. If withdrawals are made, the funds should only be used to meet ends' need and should never be spent for lifestyle purposes.

When dusts are settled, consider to build your stash of emergency funds to avoid the need to tap into retirement funds again should similar crisis occurs in the future.

Similar with reduced mandatory contribution rate from 11% to 7% introduced in March 2020 as part of the economic stimulus package designed to encourage domestic consumption, the mandatory contribution rate remains reduced albeit at the rate of 9% throughout 2021.

Employees are given option to opt-out from the reduced rates, which I believe most (if not all) of us should stick with the old 11% rate as these are our forced-savings for our own good during retirement years.

Personally, I opted-out from the reduced rates during 2020 but will be doing something different in 2021 - by accepting the lower mandatory rate. I am only doing so as I am confident not to spend that extra 2% cashflow but instead, I will divert all of it into my international ETFs under my personally-managed portfolio.

Nevertheless, 2% may not mean much but it is just my little attempt to further diversify out from Malaysia by aggregating the sum into my existing monthly contributions to international ETFs.

I hope that this article have provided you more insights on how you can look at EPF as part of your Core Portfolio which will play a crucial role in your retirement years. Their Strategic Asset Allocation (SAA) framework have primarily been designed to preserve members' capital while enhancing the value through consistent and sustainable growth. With this, I am relying heavily on EPF as the anchor of my overall investment portfolio and this have allowed me to pursue higher overall risks on my personal investments.

As much as possible, I strongly believe that one should avoid dipping into their EPF savings for expenditures, unless if there are really no other means to meet ends' need. Always remember that EPF will be your core retirement nests and plan carefully before deciding your next course of actions.

To better make an informed decision, always consider your current investment horizons, risk appetites and portfolio allocation. From there, you will have to assess what are the most suitable options which will work for you. Always do your own research, assessing your personal circumstances to come out with a personalised plan suitable for yourself.

In general, if you have no idea what you are doing, you probably should not even touch your EPF funds and let EPF manage it for you which they've consistently been doing a great job for the past 50 years.

As always - thanks for reading and see you again in my next post! If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie