Whenever we happen to land on topics surrounding Interest Rate with my friends or colleagues during our chit-chat sessions - I am still surprised with how many of us out there whom still do not have a good grasp on the concept of Simple Interest Rate vs. Effective Interest Rate vs. Compounded Interest Rate.

A typical conversation around interest rate can go like this.

Person A: "Eh, nowadays the interest rate for car loan so cheap, only 2.5%!"

Person B: "Oh really? I also want! You taking 5 years or 9 years?"

Person A: "9 years la of course. Cheaper than housing loan leh, Housing loan also 3.5% to 4% already!"

That's the part where I typically will try to jump in and explain the mechanics on how simple interest rate do not take into consideration the compounding effects - and usually most people are lost. Especially since that there’s a ton of calculations involved and may be tricky to have in casual conversational setting without given sufficient time.

We have probably always heard about it - the word "interest rate" that can either make one cry or smile - depending which side of the fences we are on. According to Investopedia, the definition for interest rate is as such:

The interest rate is the amount a lender charges for the use of assets expressed as a percentage of the principal. The interest rate is typically noted on an annual basis known as the annual percentage rate (APR). The assets borrowed could include cash, consumer goods, or large assets such as a vehicle or building.

Investopedia

In a nutshell, interest rates are typically applied on top of principal borrowed from the lenders (i.e. banks). To put it simply, when you choose to take up a loan, lenders/banks will apply interest on top of your original loan amount as part of their profits – a key and importance strategy for lenders to make money.

Unfortunately, when lenders advertise their loan packages, they use several different methodologies (or terminologies) to advertise the interest rates which may paint a rosy picture for those without good financial understanding. There’s quite a number of definitions, just to name a few:

Hence it is not surprising that many people may get confused easily (myself included at one point) unless they have strong finance background or if they have started looking into this topic. To make things worse, you also have mortgage-specific terminologies in Malaysia such as:

I will leave the mortgage specific rates on another article – but the easiest way to put it is where by adding or subtracting a certain % from the Base (Lending) Rate, you will in most cases get the Compounded Interest Rate (also known as Effective Interest Rate / Reducing Balance Rate).

There’s also slightly advanced topic such as Rule of 78 when it comes to car / personal loan, but I’ll them leave out from this article for now just to keep things simple.

So, what does it really mean to have multiple interest rates definition? It means that we can never take things from the surface level and due diligences must always be made to find out the true story behind the numbers.

Assuming that there are two different loan offering 3% interest rate, the “true interest paid” may differ based on which interest rate are stated (nominal or effective? Flat or reducing balance?). The most important factor to take note is how the interest is calculated using which number as the ‘baseline’.

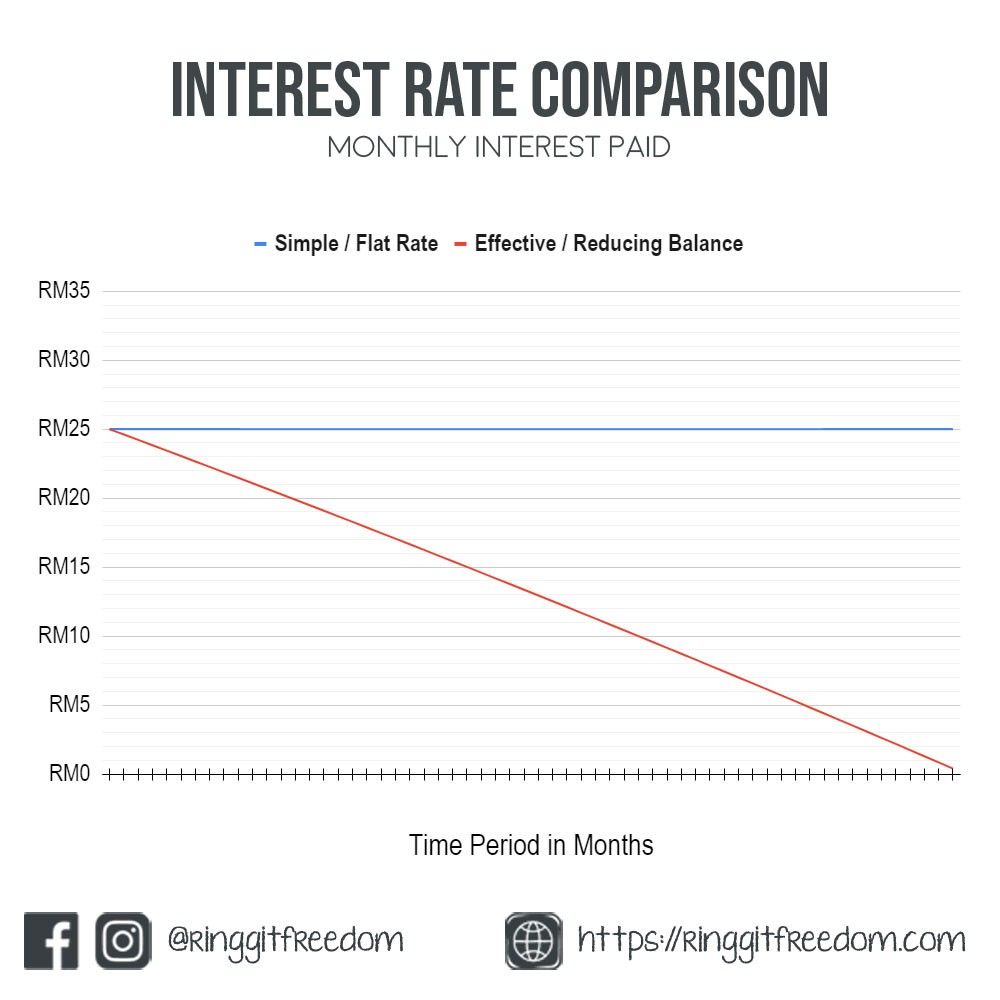

Simple Interest Rate, in other words, nominal interest rate or flat rate calculation. If the interest is calculated based on the original principal amount regardless of current repayment period, then most likely we’re looking at a simple interest / flat rate calculation.

In simpler words – simple interest, as its name imply, keep things simple by neglecting the compounding effect and assumes interest calculation based on original principal throughout the repayment period – irregardless how much you have paid up so far.

This is most commonly found in most personal loans or car loans, though banks may introduce advanced concepts to accelerate their interest collections during the early loan tenures (e.g. Rule of 78). The most obvious disadvantage is that you tend to "lose out" even if you choose to make extra payment - because your interests are always calculated based on the original principal amount.

Put it simply, you've already agreed upfront on the amount of interests to be paid when taking up the loan. Even if banks may provide "discounts" or "rebates" if you choose to repay the loan earlier, you may end up not saving much due to the way banks typically structure their loans to maximise interest collection early on (more on this advanced topic for other day).

Simple Interest Amount = P * i * n

Where

Equated Monthly Instalment = (P + S) / n

Where

As its name imply - simple interest is also very simple to calculate. To better illustrate the point, say we took up a 5 years loan of RM10,000 from a bank with simple interest of 3% per annum, on a monthly repayment scheme.

To calculate the interest payable,

SIMPLE INTEREST AMOUNT =

P * i * n =

RM10,000 X 3% X 5 YEARS =

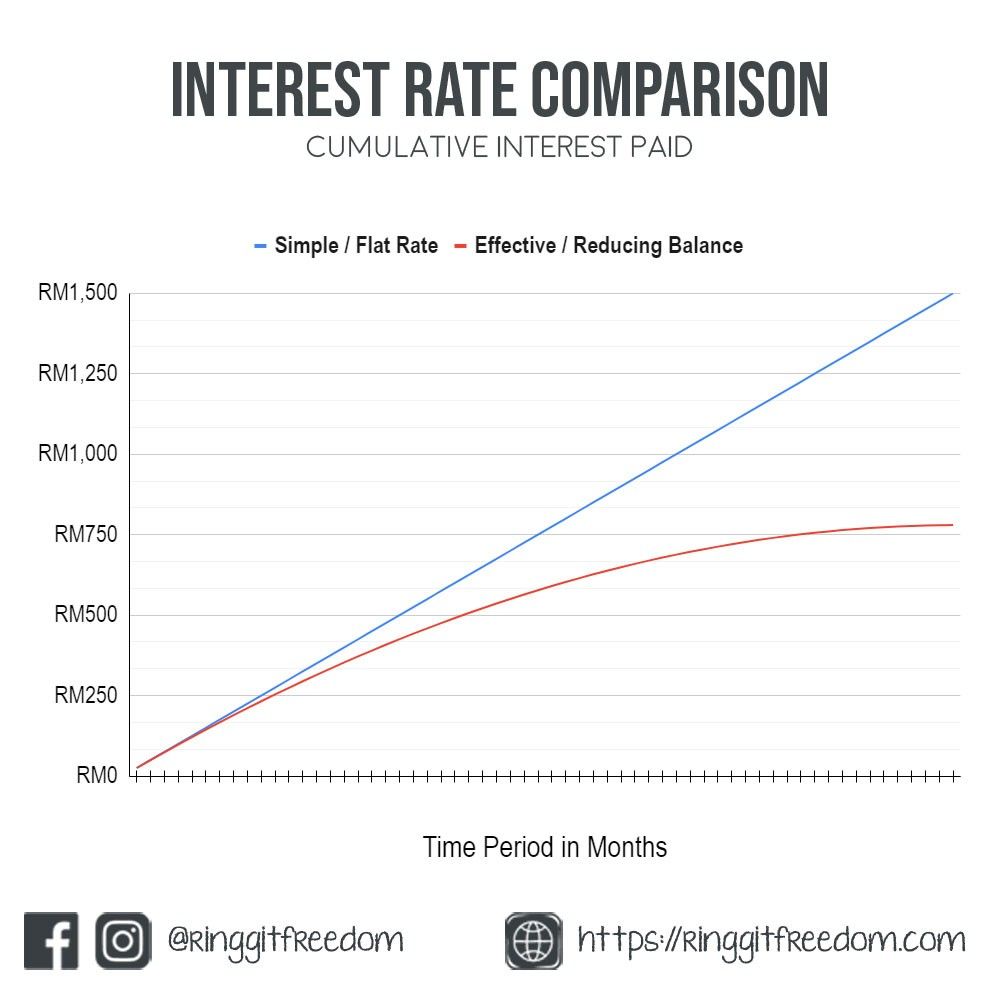

RM1,500

Add that amount of interest to be paid on top of the principal, and you'll get the total amount payable. Once you have the total amount, simply divide it by the total repayment period over 5 years (a.k.a. 60 months), and you'll get the monthly instalment amount.

EQUATED MONTHLY INSTALMENT =

(P + S) / n =

(RM10,000 + RM1,500) / 60 =

(RM11,500) / 60 =

~RM191.67

This means that we will need to repay the bank with an instalment of approx. RM191.67 monthly.

If you are interested, check out this Google Sheets illustrating the detailed calculations above with amortisation schedule.

If the principal used to calculate the interest reduces over time in tandem with the current repayment period, then we are looking at effective interest / reducing balance calculation.

It takes into consideration the compounding effect from the reducing principal balance owed over time, hence the term “reducing balance”. This will in return reduce the interests payable over time.

We will usually see these in Mortgage loans - as the amount involved are huge and if simple interest calculation are applied, the amount will be crazily enormous and it will simply make no sense to take up mortgage loan to purchase homes.

Equated Monthly Instalment = (P * i * (1 + i)n ) / ((1+i)n)-1

Where

Effective Interest Amount = (EMI * n) - P

Where

Using a similar example, in this case, we took up a 5 years loan of RM10,000 from a bank with effective interest rate of 3% per annum, on a monthly repayment scheme (a.k.a 60 months)

To calculate the total effective interest amount, you have to either do it backwards by first calculating the equated monthly instalment (EMI) amount - or calculate individual period manually. Either way, it's a mess.

EQUATED MONTHLY INSTALMENT =

(P * i * (1 + i)n ) / ((1+i)n)-1 =

(10000 * (3%/12) * (1 + (3%/12))^60 ) / ((1+(3%/12))^60)-1 =

29.04041954 / 0.161616782 =

~RM179.69

From here, you can then calculate the total effective interest amount

EFFECTIVE INTEREST AMOUNT =

(EMI * n) - P =

(RM179.69 * 60) - RM10,000 =

~RM781.21

As you can see, compared to the previous example, you are only incurring ~RM781.21 worth of interest (vs. RM1,500 earlier). Even though both have 3% interest rate, but due to the different methods used in calculation, you are effectively paying less with this reducing balance method.

If you are interested, check out this Google Sheets illustrating the detailed calculations above with amortisation schedule.

By definition - both "effective interest / reducing balance calculation" and "compounding interest" follows the exact same theory. This is merely an "extended" topic from the above chapter.

In some special cases, bank may combine the reducing balance calculation with additional compounded interest rate - or otherwise known as "Interest-on-Interest". This concept is exactly the same of Effective Interest Rate - with only one differences where interests incurred are allowed to be "compounded" on top of the balance principal - exactly the same concept why compound interest (for investing) can be so powerful.

This is common in scenarios of outstanding credit card balances, where any "finances charges" calculated, if not settled, will be added back on top of your principal balances hence resulting in longer repayment periods.

This is why you always see lengthy explanation on the back of your credit card statement explaining the concept of higher interests accrued if card holders only make minimum payment - and why they will always enforce minimum 5% payment. Otherwise the compounding effect will be more than enough to send debtors into infinite loop.

p/s try flipping this scenario and replace "credit card" with "investments" - and you'll see the reason why we've always been going on and on about the power of compounding effects.

Assuming that you currently owe bank RM10,000 with 18% per annum on outstanding balances incurred as Finance Charges.

On the first month, the finance charges of RM150 will be added on top of your principal - awaiting for your repayment hence the total owed to the bank will be RM10,150.

When next month comes, the "finance charges" (a.k.a. compounded interest) will be calculated on your outstanding balance. This is why bank enforces minimum 5% payment (or RM50, whichever is greater) otherwise your single debt of RM3K can compound into infinity.

If you are interested, check out this Google Sheets illustrating the detailed calculations above.

I hope that this article has helped you to better understand the differences between simple interest (flat rate) and effective interest (reducing balance), together with compounded interest (interest-on-interest).

The two most common underlying principle will be the flat rate (simple interest); followed by reducing balance (effective interest). Compounded interest on the other hand is basically just an extension of reducing balance, by compounding interest on top of interests - adding it onto the principal.

The next time before you decide to take on any loan, make sure to go through the details and understand the type of interest calculations applied on your loan. Some loans also have specific clauses on handling of early or additional repayments and its effect towards principal balance – always read before signing the dotted lines!

If there's at least just ONE key takeaway that you should remember - effective/compounded interest rate is basically your friend, when used correctly. It allows you to compare various financial product offerings - from loans to investments, as it provides you with the "true" interest rate adjusted for compounding period.

This is also the whole reason why starting investment as early as possible are beneficial for us - as we're having Compounded Interest to work in our favour rather than against us (in the case of Credit Card finance charges).

As always - thanks for reading and see you again in my next post! If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie