While I did not sit around when the #Budget2021 was announced live over the evening yesterday, thanks to the power of social media and the beautiful summary done by KPMG Malaysia, I got up to speed rather quickly

I won't be discussing much on the macro-economics part of the #Budget2021, but instead I will be focusing more on the impact to our personal income tax, and zooming in some of those easy (and almost guaranteed) benefit for most of us with minimal criteria. But first we need to know what are the changes made to our personal income tax for year assessment (YA) 2021 onwards

Generally I will be splitting them into two main categories, based on the policy's duration whether if a fixed period was specified ("Temporary") or if it an open ended ones ("Permanent"). Of course the government will have the right to amend or cease something the following Tax Assessment Year ("YA").

I know most items above are in super high-level - if you're keen to know more about the tax relief / changes in detail, check out summary done by KPMG Malaysia,

By now you may have already noticed - I highlighted some of the items in red above and you might have guessed it already - those are the ones I will be focusing on today!

As always, let's start with the easy one first:

As long as you are earning at least RM5,833.33 per month, it'd be a RM200 cash in the form of "tax reduction". Based on studies from Department of Statistics Malaysia (DOSM), 50% of the household (M2 and above) would hopefully enjoy this benefit (hence the "median" income)

In short, 4 additional years for us to get tax relief based on contributions into your private retirement funds. One easy way to calculate? (I use it all the time to convince others to PUT MONEY IN PRS to save on taxes legally)

multiply RM3,000 with your highest tax bracket

See how the savings go up as your in tandem with your income bracket? Now think about what will happen when you reinvest and compound these savings until your retirement age.

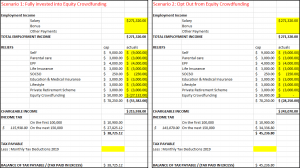

Now to me, this is really the interesting one. Or at least it intrigued my interest enough to start reading more about Equity Crowdfunding and to understand its concept - I have at least half a year to think and plan it, eh?

The concept is simple, up to 50% of your capital invested into Equity Crowdfunding will be exempted from tax, hence reducing your chargeable incomes, capped at RM50,000 or 10% your aggregate income (whichever is lower). However the upfront capital required would need to be significant enough to actually create an impact to the savings.

Take an example Mr Beans being a T20 earner in Kuala Lumpur earning RM22,610 per month (source: DOSM), with take-home-pay of RM16,016.15.

Based on his aggregate income of RM271,320, he can potentially go for tax exemption up to RM27,132 which means that he'll need to invest at least RM54,264 into Equity Crowdfunding companies.

Assuming he have an aggressive savings rate of 50%, he'd get approx. RM8,000 savings per month (rounded) which will net him with RM96,000 for investment purposes throughout the year.

To maximise the tax relief, he would invest RM54,264 out of RM96,000 from his savings; which also means that 56% of his investment will go into Equity Crowdfunding. Let's assume he went ahead with it - the upside that he will get immediately is a net tax savings of RM6,511.68, or approx ~12% ROI sponsored from the Government, assuming typical individual tax reliefs claimed.

This example is obviously biased - as we're talking about Mr Beans whom are part of the "top of the top" T20 group. While the realised benefit will still be in tandem with your corresponding tax bracket - it also begs the question: "with lesser pool of money available to invest, there must be many other alternatives out there where one can first capitalise?"

For me at least, that's a huge risk that I personally would not pursue for a few reasons:

Well at least one thing turned out well from this #Budget2021 announcement - I researched slightly into Equity Crowdfunding and decided that it's not for me yet at this stage. So we'll see next time.

This opinion piece went longer than I initially thought it would be, but I hope it was useful to you! Let me know in the comments below if there's anything else in particular that you'd like to know, and as always, see you in my next post!

If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie