As much as we'd hope that Ringgit Malaysia (MYR) will be recognised by more global institutions, unfortunately it has yet to reach such globalised status that our peers currently enjoy being Asia's Hub - the likes of Singapore Dollar (SGD) or Hong Kong Dollar (HKD).

Hence it's not surprising to see that most international brokers will have presence and acceptance of local transfer in those currencies / country, but not for Ringgit. Of course, there's alternatives like international telegraphic transfer (which are super expensive and simply not worth it) or Fintech transfer (via likes of Wise or Instarem) which some global institutions will reject third party transfers under others' account name to avoid potential money laundering (tho some are willing to accept if you provide proof of money trail)

As such, it's always good to have an offshore account either to keep your proceeds in a stronger currency, or just to use it as in-transit account under your name. This guide will is part of International Investing series where I covered on how I explored and selected my international brokerage for overseas investing, For now, I'll be focusing more on how Malaysians, in general, can apply for Offshore bank accounts at the comfort of your desk.

Technically speaking, I didn't need to open another offshore account as I already have my Hong Kong account back in the days when I was still working overseas for a short period. I chose not to close the account when I was repatriated for the convenience that it might bring me in the future (and indeed it was a good decision for me). Ironically I completely forgot about it when I was so fixated on researching the steps to open a Singapore Account

Let's get started!

Before I decided to go ahead with CIMB Singapore, I've done some research and compared the two products - Maybank Singapore iSAVvy vs. CIMB Singapore FastSaver. Frankly speaking, both accounts are pretty much the same if you only intend to use it for in-transit account.

| Maybank | CIMB Bank | |

|---|---|---|

| (Paper Form via Malaysia Branches only) Update 2023: Now available via Online Form | Application Process | Fully Online Form |

| SGD$1000 | Minimum Initial Deposit | SGD$1000 |

| SGD$500 | Minimum Balance | SGD$0 |

| $2/month fall-below fees | Fees (min. balance) | $0 |

| $10 - waived | Fees (inward TT) | $0 - waived |

| 21 or more | No. of Branches | Only 1 🙁 |

Based on my needs, I didn't need the flexibility of ATM Withdrawal in Singapore at this stage (yet) so CIMB is more than sufficient for me, plus it's convenient, free, and no minimum balance to deal with - hence an obvious choice for me although I'm more active with Maybank than CIMB bank back home in Malaysia.

Another thing to consider (if you are using this as transit account for investment) is if there's any withdrawal from your investments onto this account, check if your brokerage does it via Local-to-Local FAST transfer or via Local Wire Remittance (Telegraphic Transfer), as Maybank charges $10 per inward transaction whereas CIMB waived it (as of now)

Your circumstances may wary so choose one that fits your need best (i.e. if you have access to Premier Banking options like HSBC Premier, etc.).

As a start, you must at least have these with you to smoothen the journey

If you already have CIMB Malaysia account with CIMB Clicks activated (and not dormant like mine), you can skip this entire chapter (or read on, if you plan to save on the annual fees).

If you don't have CIMB Malaysia account yet, you can either opt for a fully-digital OctoSavers Account-i (which is also Shariah-compliant) or the Basic Savings Account 1, both which has zero annual fees.

Personally I'm still holding their traditional Basic Savings Account 1, which provides an option to have a zero-annual-fees. You just have make sure to keep it active and not let it become dormant, as I've had mine dormant twice had to pay penalties to reactivate the account. If you are planning to withdraw (via ATM) very frequently, then you have to evaluate other options (maybe Account 2 is more suitable for you).

CIMB Malaysia also have an online application process so you can just go through with the flow, but from my memory, you'd still need to visit the branch to collect debit card, activate new PIN via ATM machine, obtain CIMB Clicks MY registration key via ATM machine.

So if you're planning to apply online, and never had CIMB Malaysia's account - I'd recommend to just go with their new fully-digital OctoSavers Account-i to save you the hassle since the card will be delivered to your doorsteps. All you need is just to apply through their CIMB Apply App (Google Playstore | Apple Appstore). Some dormant customer reported issues applying their the CIMB Apply app and in those cases, you might have to pay their branch a visit - but no harm trying first!

Generally there are five parts in this section. I'll be sharing a top line summary so that you get a rough idea on what you need to go through, followed by a detailed step-by-step walk-through guide.

Time needed: 10 minutes

Summary steps to open CIMB SG FastSavers Account:

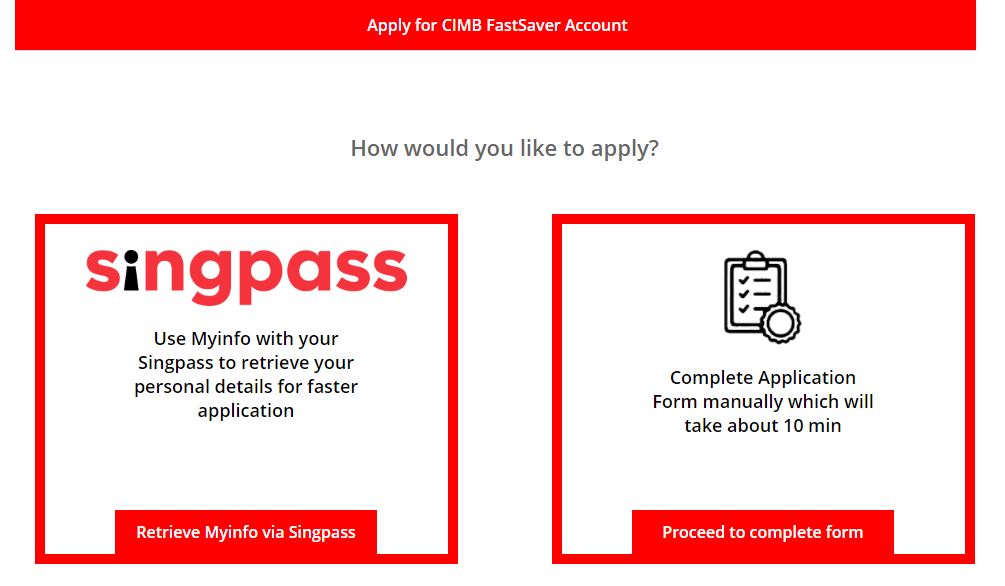

One of the easiest Singapore bank account for Malaysians to apply - through fully online application!

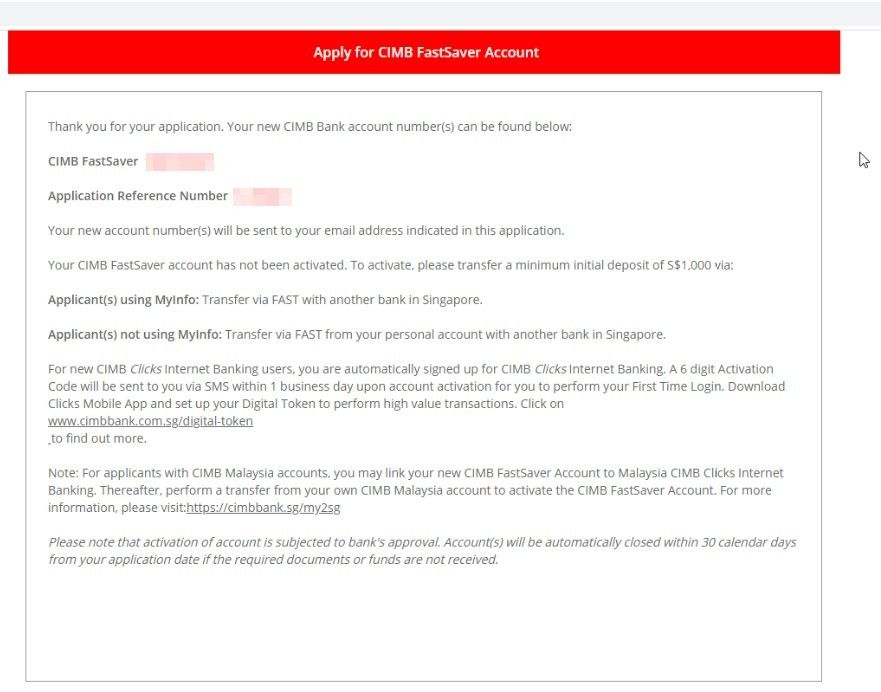

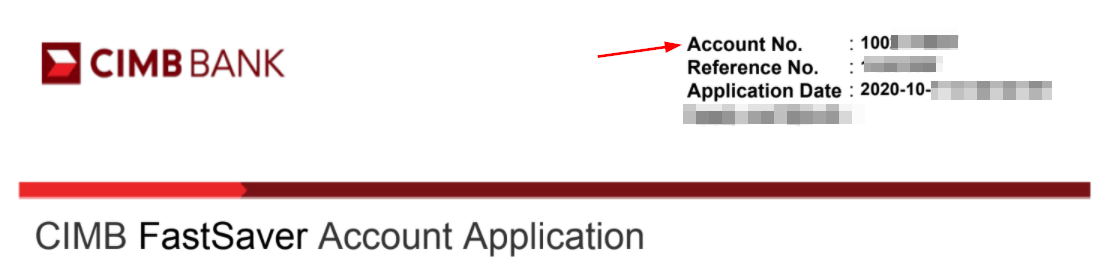

Apply for CIMB FastSavers account through CIMB Singapore website. Don't forget to write down your application reference & bank account number upon completion!

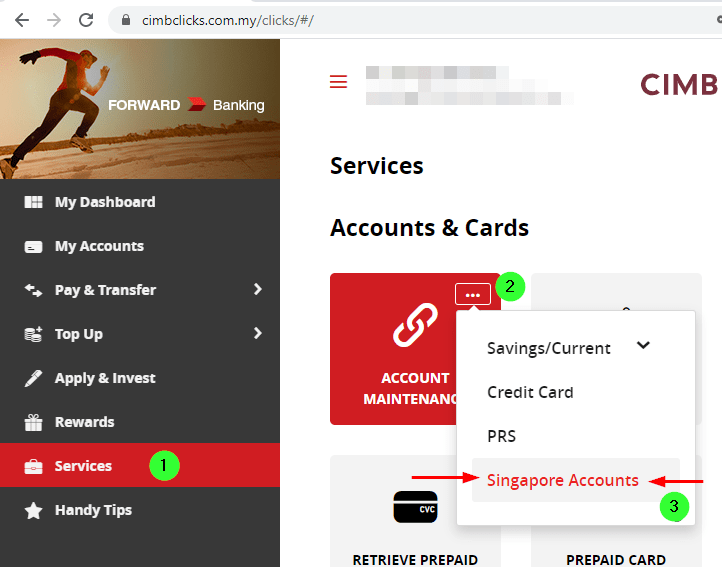

Establish the account linkage between your Malaysia and your Singapore account - allowing you to see your Singapore account through CIMB Clicks Malaysia and also transfer at competitive rates.

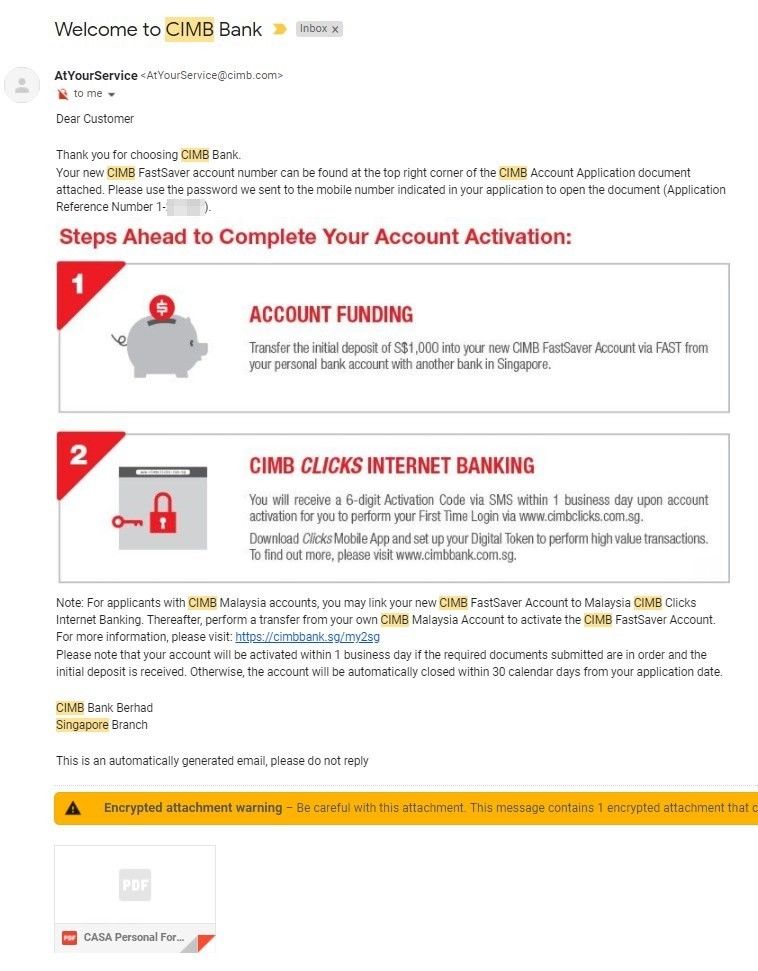

The account opening requires a minimum of SGD1000 initial funding, which you will need to complete the funding process within 30 days.

As with all financial industries, there will be mandatory 'Know Your Customer' checks. You can do this remotely as long as you linked your Malaysia and Singapore accounts.

Once your account is fully approved - you will receive access to CIMB Clicks Singapore. Don't forget to download their CIMB Singapore apps on your mobile phone, to serve as a Digital Token / TAC Security Device!

I've documented the detailed step-by-step walk-through below and hope that this will be useful for you!

Important Note: Once you initiated step 1, you have to complete the rest of the steps within 30 days or risk automatic application closure/cancellation.

For Shariah compliant account, you can opt for CIMB SG FastSaver-i instead.

Prepare also your proof of IC, residential address, and e-signature ready with you.

It is strongly recommended to open Singapore Account with your Malaysian NRIC to ease the linking process between Malaysia & Singapore with the same NRIC Number.

If you are a tax resident (i.e. tax submission to LHDN), ensure that you declare it under the CRS Reporting section and provide your Tax Identification Number (TIN) - which basically is your LHDN Income Tax File Number.

Useful Links

Non-Shariah Compliant: CIMB SG FastSaver Product Page

Shariah Compliant: CIMB SG FastSaver-i Product Page

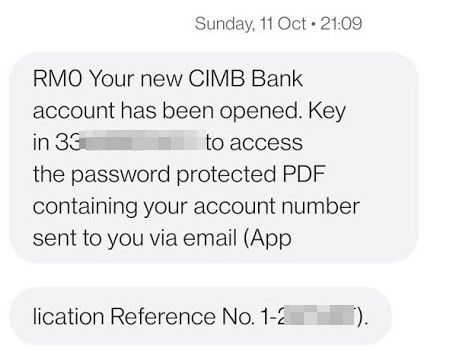

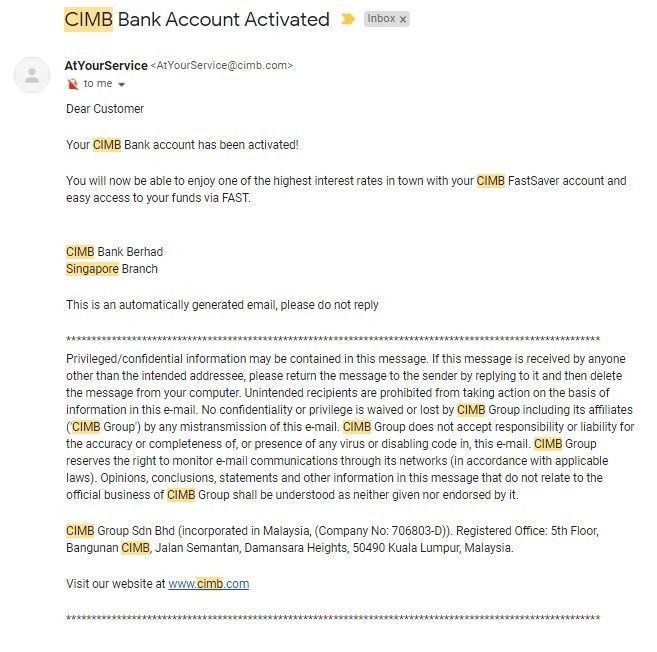

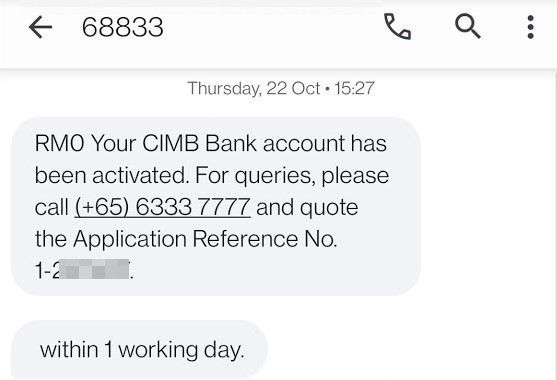

Which should contain your CIMB SG account number & application reference number

When you open the PDF, you will find all your details submitted during the application and also your CIMB SG account/reference numbers.

Some people reported that they did not receive this SMS in step 3. If you have already written down the account number/reference number during step 2, then this won't be a problem for you. Otherwise, you will have to contact CIMB SG customer service to get your account number.

This step is mandatory before you can perform e-KYC verification (online) without visiting Singapore Branch.

Since you already have an account opened in Malaysia with your NRIC, linking your CIMB Singapore account to your existing CIMB Malaysia Account allows you to perform "own-account local transfer" within CIMB Clicks Malaysia, which in turn allows the Singapore team to complete the e-KYC verification process by cross-validating your identity in Malaysia Malaysia vs. Singapore without your physical presence.

Login to CIMB Clicks Malaysia, find "Services" page (only visible on Desktop) and select "Link Singapore Account" under Account Maintenance section.

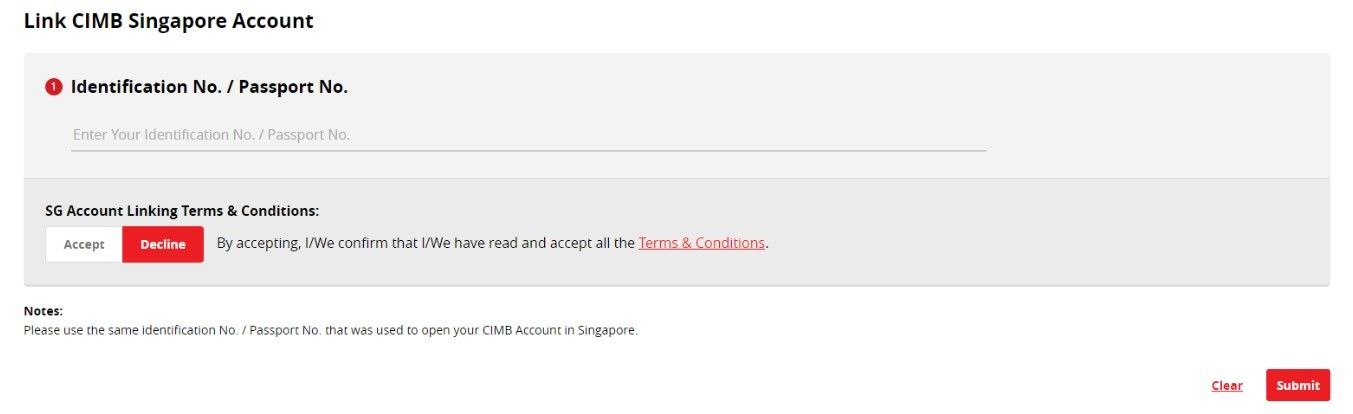

Once you are here, just input the NRIC number (or Passport number) you have inputted during the CIMB SG account opening application process.

If you choose to skip the above steps, the only alternative for them to validate your identity is to physically visit their branch in Singapore (which is impossible for most of us). This helps them to perform checks for anti-money laundering & fraud prevention.

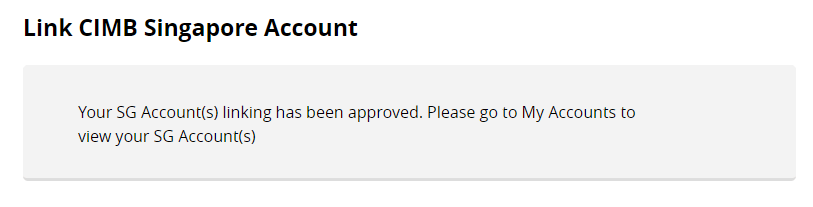

To check on status, follow the exact steps listed earlier (click Singapore Accounts) and it'll show you the status (pending approval)

If for whatever reason, it shows the input screen again (like the ones you saw in step 4), that means your application has been rejected.

I had the same issue as well - call up the Malaysia Customer Service and explain to them you need to have this account linked, to perform ASEAN Transfer for e-KYC verification requested by the Singapore team.

Whatever you do, DO NOT ATTEMPT Telegraphic Transfer - not only it's expensive, it is not recognised for e-KYC verification as these are treated as 3rd party transfer (and not first party own-account transfer). I've paid for my lessons 😀

UPDATE 11/5/2024: There have been several reports that the CIMB SG will call you to request to perform a full SGD$1,000 transfer via CIMB Clicks - so you may skip step 6 altogether and only use it for your FUTURE transfers to save on exchange rates.

Or do it after linkage approval to minimize the days' gap between funding & e-KYC (important! read updates below)

To further explain, to meet the SGD$1,000 account opening requirement, the source of fund is more flexible as long as it comes from yourself.

It does not necessarily need to be funded from CIMB Malaysia as the rates can be expensive even with the fee-waivers of ASEAN transfer (not Telegraphic Transfer) made available after your CIMB accounts are linked.

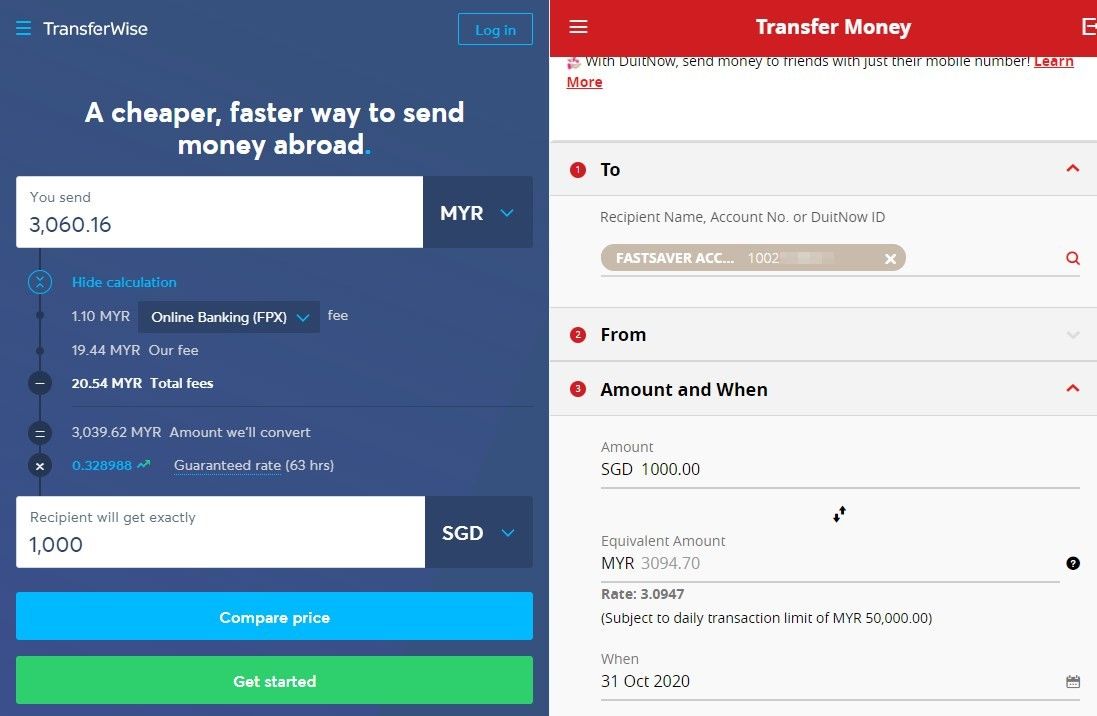

I personally would recommend using Fintech transfers like Wise (formerly known as TransferWise) or InstaReM to save on international transfer fees. At the time of writing, to fund 1K SGD it will cost me approximately RM3,060.16 (Wise) vs RM3,094.70 (CIMB Asean Local Transfer).

p/s feel free to use my referral for Wise to support my blog! For every successful referral, part of the commissions will go to a non-profit community charity foundation.

UPDATE 9/6/2021: There seems to be a new clause added on CIMB SG FastSaver website, implying that initial funding must be from CIMB Malaysia or other Singapore accounts under your own personal name.

From my understanding with CIMB SG, as long as we ensure to perform step 7 e-KYC process on a timely basis, with at least SGD$1 Local DuitNow Transfer from CIMB CLICKS Malaysia to your Singapore account; there should not be an issue with the funding. This clause was added recently as there were many non-compliant applicants completely skipping the e-KYC process resulting in a refund.

Should there be further developments or new discoveries on this topic, I will be updating this post accordingly.

UPDATE 11/5/2024: There have been several reports that the CIMB SG will call you to request to perform a full SGD$1,000 transfer via CIMB Clicks - so you may skip step 6 altogether and only use it for your FUTURE transfers to save on exchange rates.

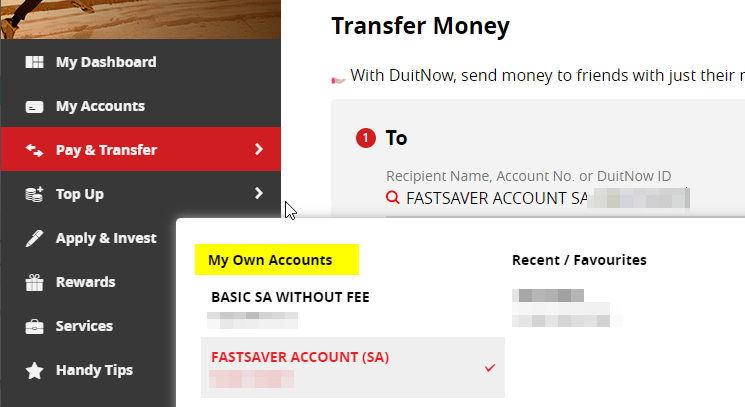

If so, simply head to "Transfer Money" (Local DuitNow Transfer, not Telegraphic Transfer) and you should see your Singapore account under "My Own Accounts Recipient".

Transfer SGD$1000 from your Malaysia Account to your Singapore Account in order to meet the requirements for e-KYC verification. In the past, I transferred SGD$5 via this approach and the rest of SGD$995 via Wise to save on exchange rates, but since 2024 this is no longer possible (at least for the first e-KYC verification)

This is where they'll ultimately decide whether to approve or reject your account opening application.

If your application gets rejected, they will refund you all the monies but so far I haven't seen anyone getting rejected yet based on the Lowyat thread & comments section in this post.

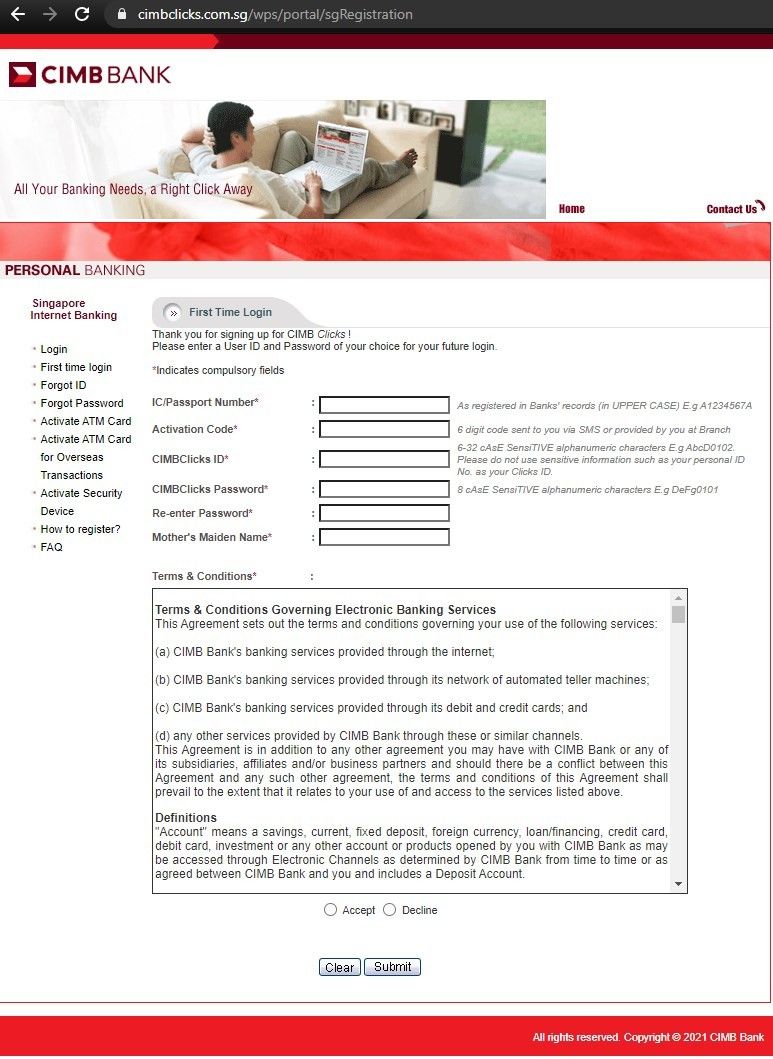

Set up your CIMB Clicks Singapore by doing the "FIRST-TIME LOGIN" and change your password via their website.

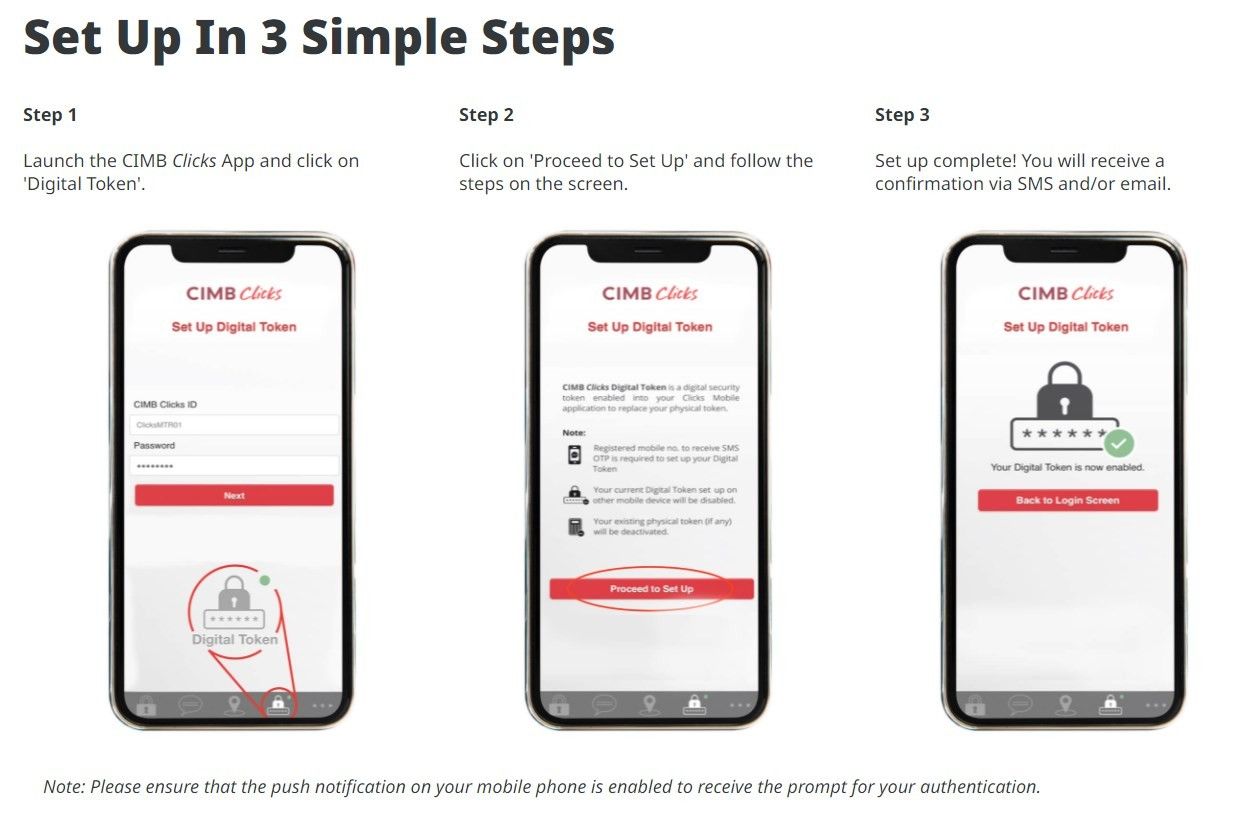

I personally recommend using their Digital Token via CIMB Clicks Singapore App (Android / iOS), which they have a detailed guide here.

It looks terribly outdated but functional enough to perform basic banking transactions. Another alternative is to visit their branch and collect your "physical token device" for OTP purposes, or request postage to Malaysia via their Customer Service.

So that's all! I hope this guide was helpful enough to get you started opening an Offshore Singapore Account whatever your reasons may be. I'll expand / update this post in the future if I ever get the chance to also explore the Maybank route, but I don't foresee it happening anytime soon.

See you in my next post! If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie

p/s in case if you'd like to support me, feel free to use my Wise referral code here and part of the commissions will go to a non-profit community charity foundation.

Special shout-out: If you prefer a video version of the step-by-step guide - check out Ziet Invests' video here!

I have decided to also compile some of the most frequently asked questions based on the PM/Comments received so far. Hope this will also be helpful for starters!

If you ever have plans to invest internationally through DIY international brokers, chances are, you'll notice that not many of them accept MYR as funding (or, MYR is included but with unfavourable exchange rate) - compared to the likes of SGD. With an international account, you'll unlock more options and freedoms of choice when it comes to funding your international brokerage accounts - ultimately saving on conversion fees.

Yes, once CIMB Singapore account is approved – you’ll be granted credentials to CIMB Clicks Singapore – make sure to have OTP mechanism in place (step 11), I went with mobile OTP via their APP.

Once that’s done, you can do FAST transfer to any Local Singapore Bank accounts, provided that the Brokerage has a presence/local bank account accepting FAST

From what I’ve gathered and seen so far – as long as you are already a verified CIMB Malaysia customer, the Singapore account opening process will be 100% online with no special conditions.

Unfortunately yes. Effective 2024, CIMB has stopped accepting partial transfers from multiple sources (i.e. CIMB MY $1 and Wise $999) hence for the first transfer, you MUST do it via your CIMB Malaysia account to your CIMB Singapore account. This transfer should be made via CIMB Clicks Malaysia website, after you have successfully linked your accounts – and performed under “Local Own Account” transfer (you’ll see both MY and SG account there if linked correctly).

From what I’ve researched so far, it’ll mostly be fine. If you are using it for investment purposes, do pay attention to the Domestic Ringgit Borrowing / Foreign Investment Asset guidelines.

Below are some useful readings related to this.

https://www.stashaway.my/faq/900000198566-what-is-domestic-ringgit-borrowing-drb

https://www.bnm.gov.my/documents/20124/60360/Notice%2B3_Investment%2Bin%2BForeign%2BCurrency%2BAsset.pdf

Please make sure that you have already activated and linked a security device to your profile. As in my case, I opted to install “CIMB Clicks Singapore” app on my phone and used it as my OTP Token Security device – since I didn’t want to go through the hassle to have physical OTP device delivered to me.

Yes, once you have completed your account opening and the initial SGD$1,000 transfer via CIMB MY, you can use whatever other sources (under your name, of course, to avoid issues with suspected money laundering) into your own CIMB SG account. Personally, I prefer to use Wise for MYR --> SGD and CIMB SG for SGD --> MYR transfer due to their competitive exchange rates.

If you have decided to stop using CIMB Singapore and you’d like to repatriate the funds back into Malaysia, similar to how you have funded it initially – you can use Wise except this time around you will transfer SGD into Malaysia. Alternatively, you can also use CIMB Singapore to perform a "Local" transfer back to Malaysia with competitive ASEAN rates (you have to link your Malaysia account into CIMB SG Clicks)

Couldn’t find much information online and I had asked customer service as of 1st April 2021. According to them, there’ll be 36 months grace period so as long as we have transactions once in a while it’ll be enough to keep the account active.

Personally I’m also only using it once in a quarter so it should be fine. Hope this help! Pasting the information from CIMB Customer Service below:

“We wish to inform that an account will turn into inactive status when there are no deposits or withdrawals performed by the account holder. Savings account will turned inactive after 36 months.

Please be assured that your funds are still in the account and will continue to earn interest.

You will not be able to transfer funds via internet banking or withdraw funds from ATM card (if applicable).

The simplest method to activate the account will be to transfer any amount from your other bank’s internet banking to your CIMB Account.

Upon receiving your transfer, your account will be activated the following day.

There are no fees for inactive account.”

It’s really up to you – just be honest and you will be fine. Most of us that I’ve seen applied selects either “Overseas Savings Purpose” or “Investment/Securities Purpose” – the exact wording are something like 'Other investment' > 'Placement/withdrawal of deposits of residents with/from financial institutions abroad'.