In one of my previous posts, I explained various different concepts of interest rate ranging from simple/flat interest to effective/compounding interest. Today, we will dive deeper into the mortgage loans available in Malaysia.

Mortgage loan for most of us, would be one of the biggest commitment we will ever have in our lifetime, typically up to the day we retire from the workforce. Hence it is extremely crucial for us to have thorough understanding before signing the dotted lines, worse if under time pressure (to avoid late payment fees charged by Developers, for example)

Personally, I was under "time pressure" back then and rushed through my researches for my entire home purchase / mortgage - trying to be as thorough and comprehensive as possible but at the same time meet the deadlines to avoid late-payment penalties from the developer. Thankfully it didn't go too bad as I was manage to work it out with a plan that suits me and walked away with only some damages (due to late payment).

I hope that with this article, it will help others whom are in midst of their journey in purchasing their first home to accelerate the understanding of home loan / mortgage as a whole, or if better, to understand the whole concepts in-depth before committing to a home purchase (don't be like Gracie).

This article will be part of my Home Ownership Series (in the future lah...). Let's get started!

As with all my articles in the past - let's start by first ironing out what exactly does a mortgage mean, shall we?

a legal agreement by which a bank or similar organisation lends you money to buy a house, etc., and you pay the money back over a particular number of years; the sum of money that you borrow

Oxford Learner's Dictionaries

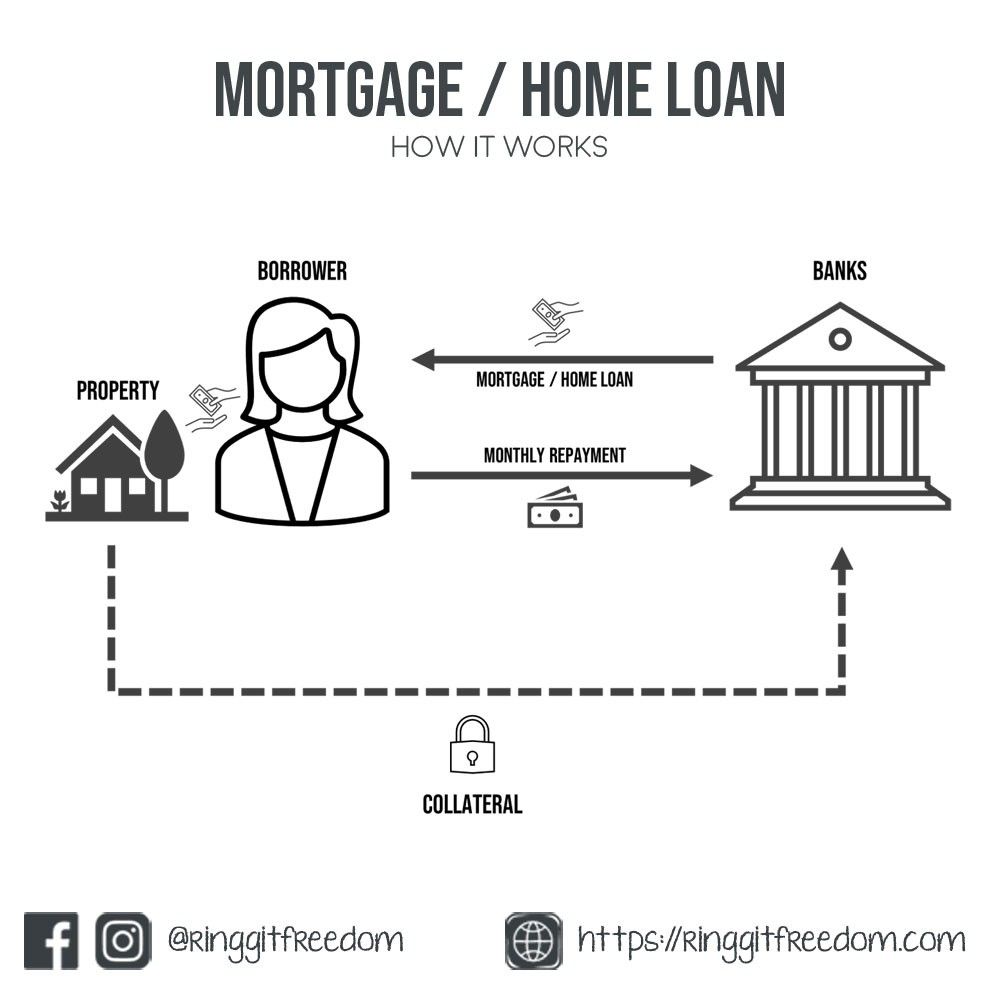

Simply put, a mortgage or mortgage loan or home loan is a type of loan provided by lenders to you, helping you to make a home purchase.

Through this process, lenders will typically require collateral to secure the loan in the event of defaults. Hence there's always a saying where the home is never truly "yours" until you fully pay it off.

In most cases, the lenders such as bank will offer up a mortgage loan package, charging an interest rate on the loan amount which may fluctuate over loan tenure in line with economic situations. The borrowers then can use the money in exchange for a property to stay in (or invested in for rental), with promises that they will promptly repay the bank over a period of several years or decades.

However, in the event of default (i.e. the borrower consecutively fails to pay back the bank the promised monthly repayment), the bank will then exercise their rights to the property putting it on auction or "lelong" to recoup the amount owed by borrowers - also known as the Property Foreclosure process.

In Malaysia, there's quite a few type of mortgage loans available for us to choose from but they generally fit in either one of these categories:

As always, there's never a one-size-fit-all solution even when it comes to mortgage loans. Depending on your circumstances, one may be more suitable for you than the other but before we get there, let's first establish our understanding on the different type of mortgage loans.

But before we move on - it's important to establish the understanding where regardless of loan types, all mortgage / home loan will be calculated following the reducing balance principle. If you don't quite understand the meaning of reducing balance - I strongly recommend to first read my previous post on Understanding "Interest Rate" Calculations in Malaysia.

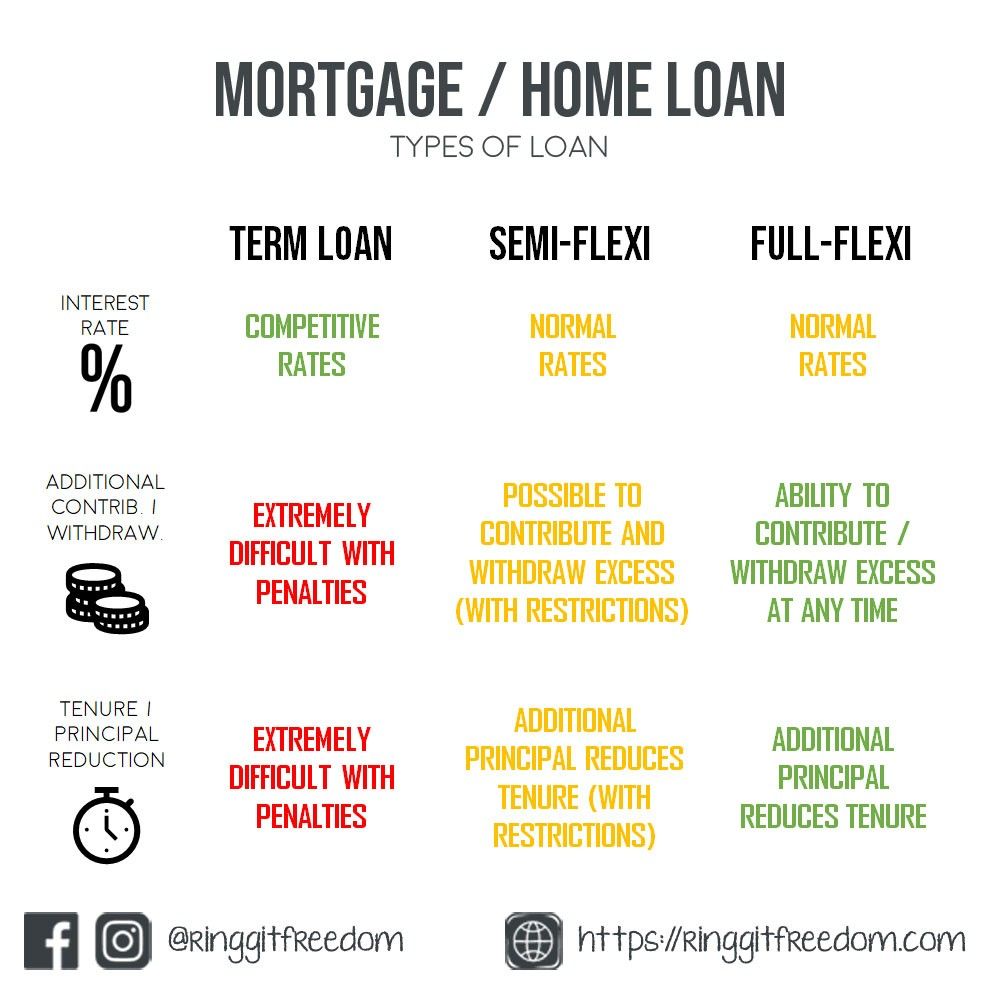

Sometimes also known as the basic loan / traditional loan. As it name implies, it is the simplest form of housing loan available where the repayment period is already calculated and agreed upfront, with fixed payment schedule throughout the tenure.

Interests are calculated on a reducing balance basis, where principal will be reduced during the monthly repayment. In case if the borrower wants to pay an additional amount as an pre-payment to reduce the capital (or full early-settlement of the loan), there will usually be penalty or fees charged as the borrower is breaching the contractual "term" on initially-promised repayment period.

Since these loan usually comes with more attractive rate than semi-flexi / full-flexi, they are most suitable for those purchasing lower-value property for investments/rental purposes already planned out their repayment periods in advance.

The case is even stronger if they also have no plans to accelerate the loan repayments due to lack of cash or plans to redirect any additional cash proceedings elsewhere (e.g. reinvested in other assets).

Similar to term-loan, the interests are calculated on the reducing balance where the principal outstanding will be reduced during monthly payments. However, semi-flexi provide the borrowers the flexibility to make an additional contributions / payments to further reduce their principal outstanding.

By doing this, it will subsequently reduce amount of outstanding principal owed hence ultimately reducing the terms required to complete the mortgage repayment as well as reducing interests charged in the subsequent month.

However, semi-flexi are "semi" because they usually come with a boatload of terms and conditions which you have to strictly pay attention to, such as but not limited to:

Still, even with some of these strings attached - it is good for those buying their property with intention to ramp up payments in the later year (in proportion to income growth) which will help them to achieve the peace-of-mind earlier by being debt-free.

As long as there are possibilities where you will plan to shorten the home loan tenure by making additional payments, semi-flexi (or full-flexi) will always be the preferred option. Note that unlike term loan, these may not have the "lowest" interest rate but reducing tenure will almost always save more interest in the long run.

The differences between semi-flexi and full-flexi is really minimal - with the one key differentiator being the less-restrictive terms and conditions / hidden strings in the full-flexi loan. It will typically still retain conditions such as early exit penalty / early settlement clause, and in most cases they will always have a monthly account maintenance fee of RM5-RM10.

As its name imply, full-flexi loan typically provides the maximum flexibility to the borrowers to make pre-payments at any time with any amount, which will directly offset the principal amount. The borrowers can also opt to withdraw any excess amount from the account with no minimums or fees charged.

Most (if not all) banks achieve this by taking the whole concept of loan account one-step further - by combining the loan facility into a 3-in-1 account which will be acting as your home loan, current account with Online Banking and ATM facility with Debit Card (i.e. Maybank Maxi Home Flexi Loan). During the month end, the bank will simply deduct the predetermined/agreed monthly deductions from your bank account along with the calculated interests.

I am currently using such home loan facility and it's really worth the convenience fees paid. Since I can transfer my payroll here and have my both my floating funds (which will be spent later) or emergency funds sitting there, it helps me to reduce my overall monthly interests charged as the interests are calculated on a daily rest basis with better interest rate than Fixed Deposits (that's how bank gets their cash to "lend" out)

The only extra thing I did was to cut-off my debit card on this account as I find it risky to use this card - considering that this is my "basket of all cash" so I'd rather go through the hassle of transferring funds to different bank's ATM card when I need to withdraw funds.

Another important concept that we must first understand - the "Amortisation Schedule". Why is this important, you may ask. Understanding the amortisation schedule allows you to better understand how your loan repayments are being structured and whether if it may potentially choke up your cash flows.

Amortisation Schedule, in simple terms, is basically your schedule of monthly repayments from first month (typically upon complete draw-down of loan amount) until the end of agreed tenure (e.g. 420th months for a 35-year loan).

The monthly repayments are the total sum paid to the lender, consisting of the principal repayment as well as interests charged. However, the exact amount distributed between principal repayment and interests charged will vary depending on which amortisation schedule are used.

Just to better illustrate the point, think amortisation schedule as a table listing the exact amount paid on a month-to-month basis, with the assumption that no additional payments were made to reduce loan tenures (for semi-flexi / full-flexi loans)

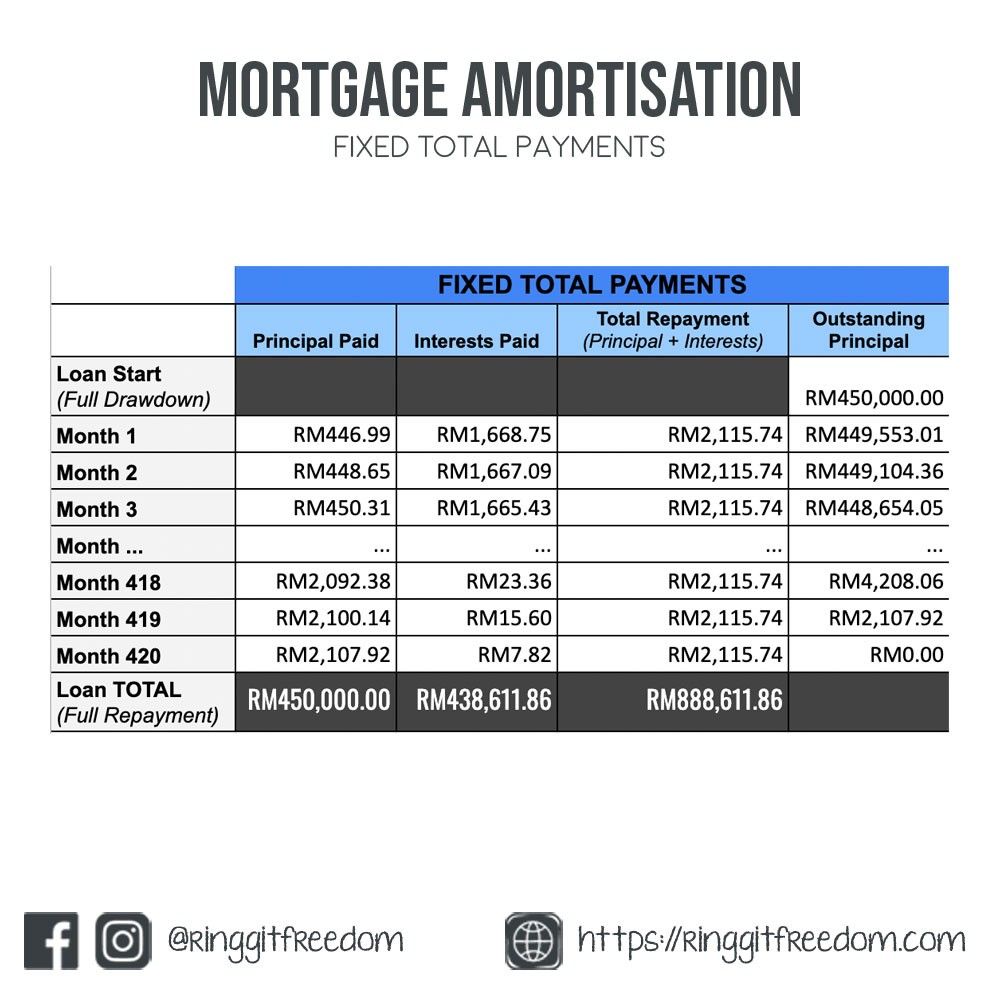

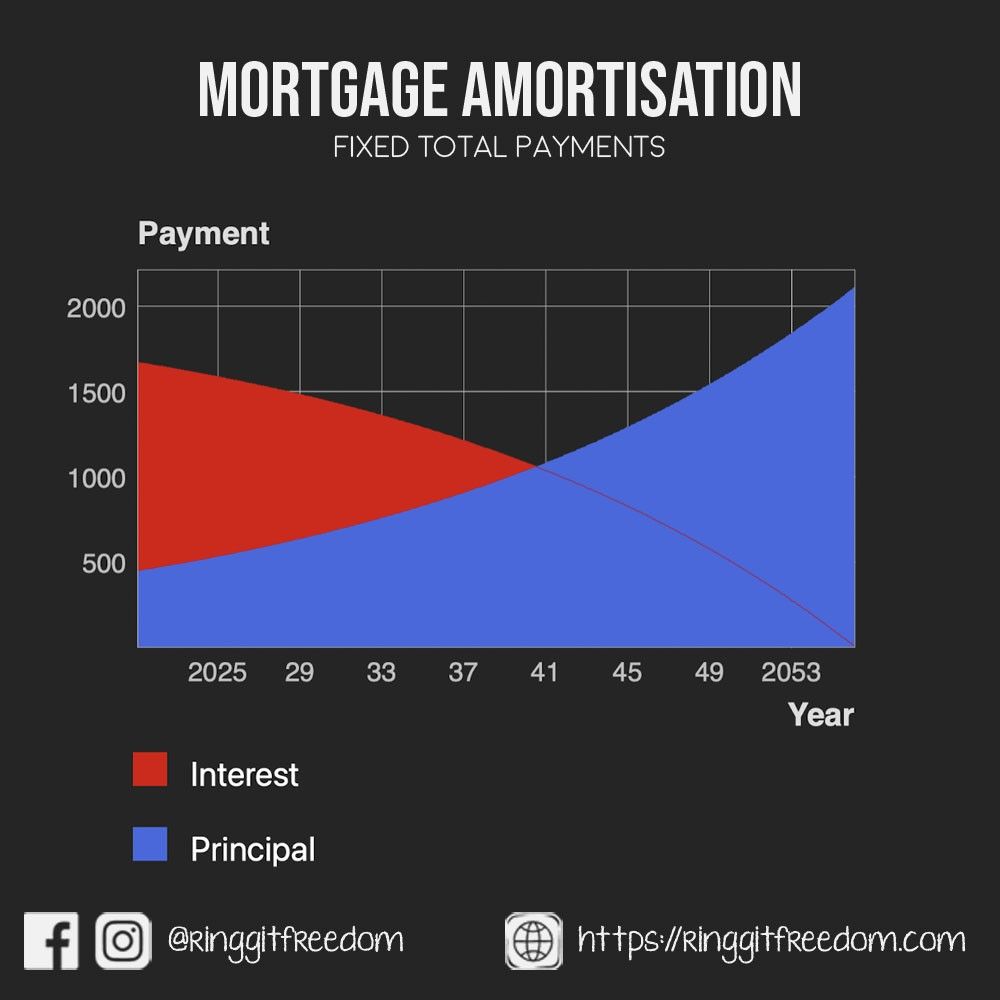

This is the most common amortisation schedule which most of us already know today. Fixed Total Payments is kinda like the de-facto standard offered by most of the banks when it comes to mortgage. In simple term, the borrower agrees to pay a fixed total amount from the first month until the end of loan tenure.

Having a fixed monthly repayment helps the borrower to accurately predict their month to month cashflow as the repayment amount stays consistent throughout the loan tenure. Having said that, while the monthly repayment is fixed, the ratio of the contribution to be spent towards Principal vs. Interests will differ throughout the loan tenure.

Unfortunately, the banks will typically weigh heavier contributions toward interest payment in the earlier months and later on gradually increases the ratio of amount paid towards principal repayment. This helps to ensure that banks will collect their portion of interest as early as possible.

For example, assuming that a borrower purchases a RM500,000 property with 10% downpayment, with the balance funded via 35 years home loan at 4.45% interest (more on interest rates in next chapter). The expected monthly repayment will be flat RM2,115.75 per month from Month 1 up to Month 420 (35 years).

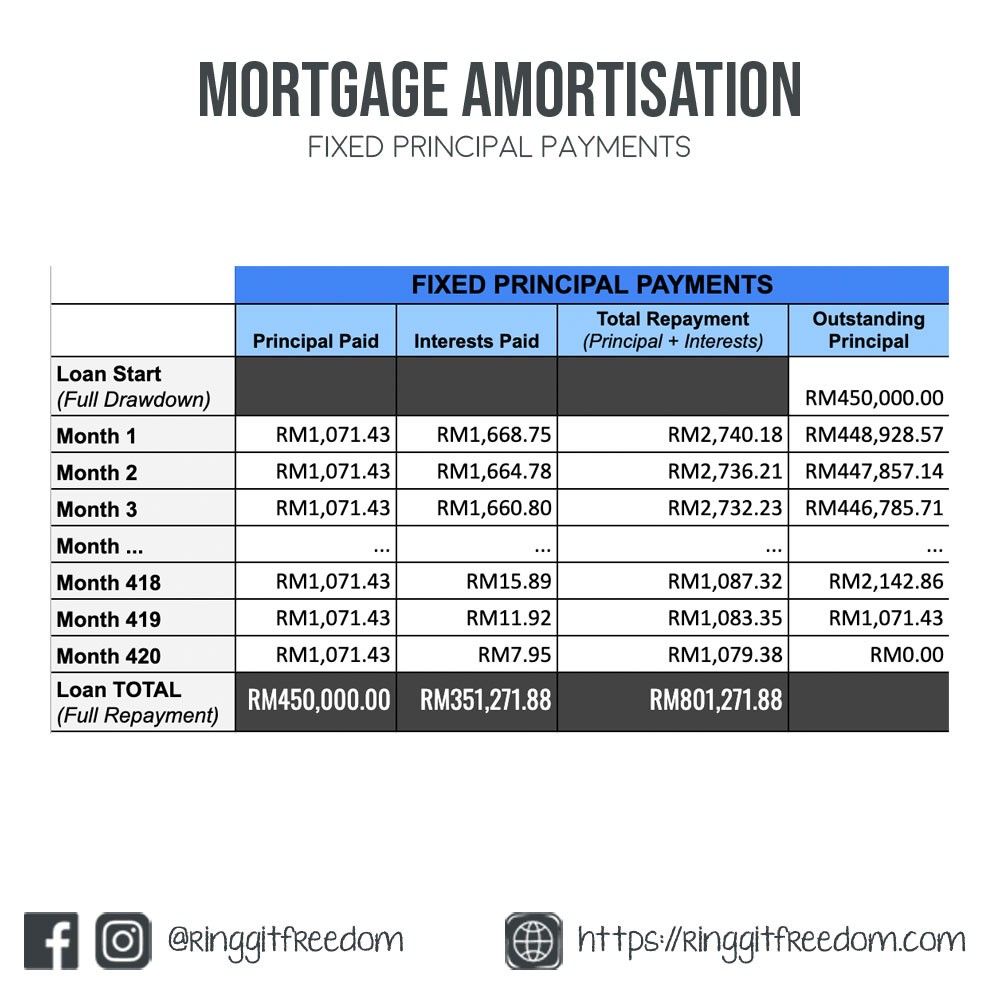

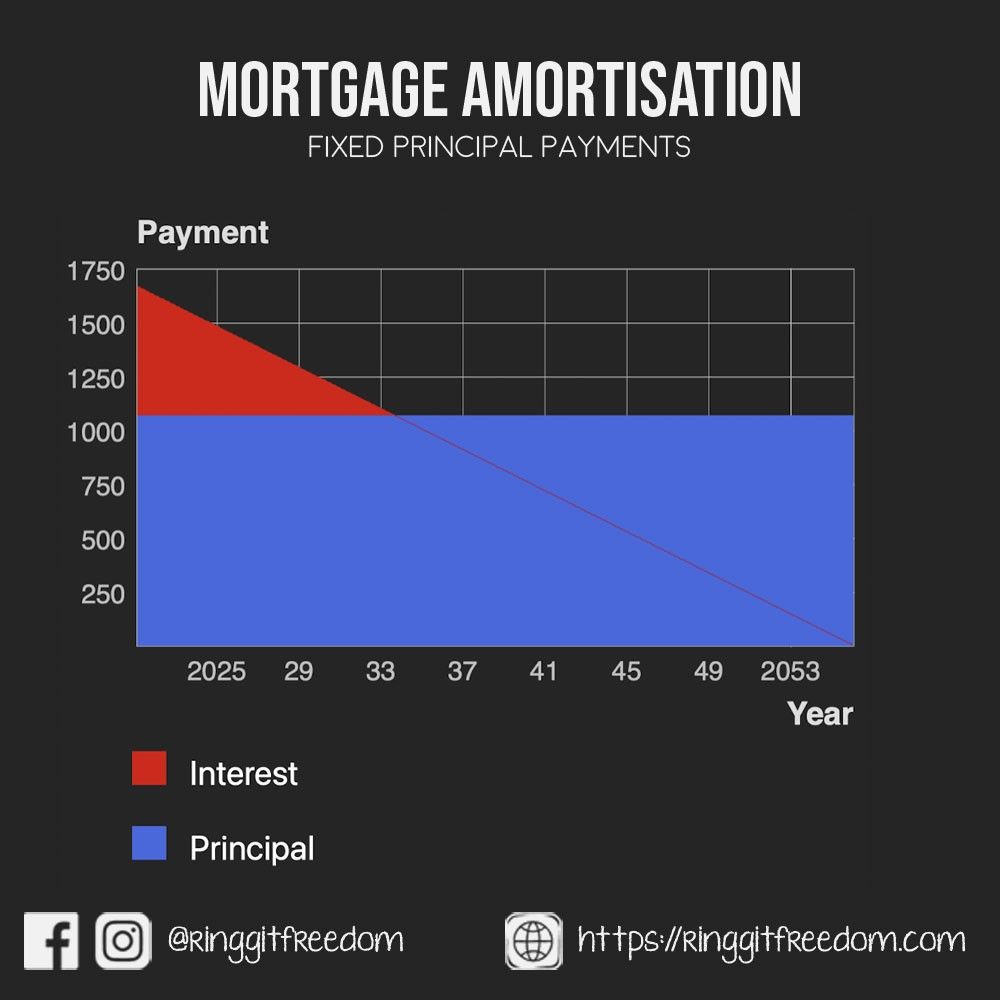

However, there's another type of amortisation schedule which not many of us are aware of - Fixed Principal Payments. Unlike the fixed total payment, this method locks down the "principal repayment" amount to be paid on a monthly basis (rather than the total repayment). On top of that, the borrower agrees to also pay interests which will be calculated based on the outstanding principal amount at that point in time.

As such, the total monthly repayment amount will vary according to the outstanding principal - since higher outstanding balance will incur higher interest charges. Due to the varying interest charges, it makes it hard for the borrower to predict the exact cash flow for the month. Since the interests are calculated on the outstanding principal, it will result in significantly higher monthly repayment during early tenure.

This may may put a significant strain on the borrower's ability to manage their cash flow. If borrowers can afford the higher monthly repayment during early years, then it may not be a bad thing at all as it will result in savings on total interests paid - since principals are reduced at a more consistent rate early-on.

If the borrower takes up semi-flexi or full-flexi loan and have the cash-flow ability to maintain "higher" commitment throughout the loan tenure, it can even shorten the total loan tenure resulting in even more interest savings!

For example, assuming that a borrower purchases a RM500,000 property with 10% downpayment, with the balance funded via 35 years home loan at 4.45% interest (more on interest rates in next chapter). The expected monthly repayment will be varying from RM2,740.18 - RM1079.38 per month from Month 1 up to Month 420 (35 years), with higher commitment in earlier months and gradually lowering the monthly repayment amount as outstanding principal reduces.

Most home loans offered in Malaysia will come with floating interest rate - which means that interest rate may change (either increase or decrease) throughout your loan tenure. Albeit rarely, there are still mortgages which are offered at fixed interest rate where the interest rate stays constant throughout the loan tenure.

Ultimately, before we go about comparing interest rates, it's crucial to first understand how these Effective Interest Rate (EIR) are calculated. If you are not sure what an EIR is, do check out my previous post on Understanding "Interest Rate" Calculations in Malaysia to at least first have general understanding on interest rates.

There are few factors that will determine interests to be charged on our mortgage, and frankly these topics itself are deep enough that it warrants an article of its own. For now, I will keep it brief enough with resources for further reading.

For banks to lend out monies to borrowers, they first must have sufficient liquidity in place in line with Central Bank's requirement on Statutory Reserve Requirement (SSR).

But what if they don't have sufficient liquidity / cash reserves from others' savings / deposits? They will resort to borrowing it from their peers (banks) and then lend the amount to you. In simpler words, OPR is basically the general interest rate bank charges one another.

Since OPR fundamentally affects the general interest rate where bank operates and gets their source of fund, any changes in the OPR will definitely affect the rest of the financial systems - including mortgages or fixed deposits rate.

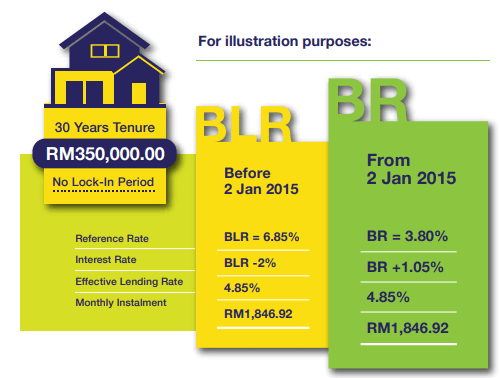

Base Lending Rate (BLR) was the de-facto standard used when advertising home loan packages, at least before January 2015 and has since been deprecated. In simpler words, Base Lending Rate is determined by the central bank based on the overall efficiency of the financial institutions across Malaysia.

Whilst the original intention was to provide a consistent and predictable interest rate across several banks - it lacked transparency to the consumers as to the spreads charged by the respective bank for consumer loans. This is especially since most (if not all) banks offered discounts to the base lending rate as the efficiency improved and competition strives.

This is where Base Rate (BR) was introduced in January 2015 to help boost transparency. Base Rate is basically the net reference rate, bench-marked against respective bank's general lending cost and Statutory Reserve Requirement (SSR). In simpler terms, Base Rate is the bank's baseline rate to "secure" the funds to be lent to borrowers.

Other components of loan pricing such as borrower credit risk, liquidity risk premium, operating costs and profit margin will be reflected in a spread above the Base Rate. In other words, these are the "premiums charged" by the bank on top of their base rate as a baseline. This increases the visibility of the factors underlying changes to the Base Rate.

In order to find out the Base Rate for respective banks, you can visit either your bank's website or Central Bank's compilation here.

What does it mean to us consumers? To get the effective interest rate of the loan, depending whether if it is BLR or BR:

Bank Negara Malaysia summarised it well with the below illustrations, which you can find more here:

What's important to remember is that with mortgage loans, unless you have signed up for a fixed interest rate package, in most cases the package would be on floating interest rate which means that when OPR goes up - so does the interest rate charged for your mortgage (and vice versa).

In the hard times of COVID-19 like today, with lowest-ever-seen OPR rate throughout the history of Malaysia, do factor in the future possibility of rising OPR rate in the long run which will result in higher interests payable for your loan repayment.

For example, when I signed up for my loan packages in January 2015, I was charged a +1.25% spread premium on top of Maybank's Base Rate (which was 3.2% in 2015). This effectively puts my mortgage's effective interest rate at 4.45% back then in 2015.

Fast forward to January 2021, with the negative outlooks projected by central bank, the OPR remains at the lowest throughout Malaysia's history and thus Maybank's Base Rate are currently sitting at the level of 1.75% from July 2020. With this, my effective interest rate for mortgage have been sitting at 3% since then which helped me to greatly reduce the interests charged.

Eventually, what goes down will come back up. In May 2023, the OPR went back up to 3.00% which makes my effective interest rate to be approximately 4.25%. Hence, it is very crucial for you to consider these factors when taking up a mortgage loan - and not solely looking at only the interest rate at the point of sign up.

Before deciding on the mortgage, aside from the more common stuff like the interest rate, l

Or in the financial world, what they call the Debt Service Ratio. Simply put, review your current budget and debts - always ensure that your total debt to be below 40-45% of your net income. General advise is to keep the monthly instalments of mortgage at maximum of 30-35% of your net income - after factoring in the possibilities of rising OPR in the future.

There are certainly many other costs when it comes to purchasing our home on top of the listed property price. Whilst I won't be able to go through all the details today, I would focus on the common offerings of financing additional costs into the mortgage (i.e. MRTA / MLTA insurance)

Before making such a decision, one important point here is to always consider the consequences of compounding interest working against you. By increasing the amount of principal owed, you will naturally incur more interests in the long run.

Even if it's just RM10K, by financing it through your mortgage, this RM10K amount will be compounded at the loan's effective interest rate throughout the tenure and you'll end up paying more interests which may even be close to double of the original amount (assuming 4.45% EIR on 35 years tenure)

There's no right answer for this as it really depends on individual circumstances. For some, the peace of mind of being debt free is worth it; but for the others, there's no mathematical reason to pay down mortgage especially if the EIR is around ~3% today, where we can easily generate investment returns above the EIR and hence putting the money into better use.

Marcus wrote a very comprehensive post on his thoughts on this subject so instead of me rewriting on this topic, I'll leave you to his post "Should We Pay Off Mortgage or Invest First?" by Marcus Keong

I hope that this article have helped you to establish deeper understanding on the topic of mortgage / home loans available in Malaysia. As with all financial decisions, you have to understand what suits you the most.

For example, if you're rotating cash flow and maximising number of mortgages of flat/apartment with good rental yield with target to pay it off within 10-15 years (as per loan schedule), and do not foresee any additional cash to be put back into reducing the loan, then getting the best Term Loan with lowest Interest Rate may be the most appropriate case.

On the other hand, if you are buying your first property (like I was back then) and are committed to reduce interest as much as possible, but requires flexibility for loan schedule just in case of active income could not catch up as quickly as expected - then a semi-flexi or full-flexi loan may be more suitable for you. Make sure to also factor in possibilities of OPR adjustments in the future which will impact the amount of interests payable throughout the loan tenure.

Don't forget to read and understand all the fine prints / clauses as well - as some loans will have petty conditions (favourable to banks, not for borrowers) embedded into the loan offer. For example, some semi-flexi imposes restriction on withdrawal and/or fees upon withdrawal; whereas some will impose minimum qualifying amount to reduce principal.

If you haven't already - I highly recommend you to download Karl's Mortgage Calculator [Apple App Store / Google Play Store] which you can play around with different mortgage loan settings which to calculate various stuff like repayment, amortisation schedule, etc. - and this will definitely helps you with better understanding.

As always - thanks for reading and see you again in my next post! If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie