Investing abroad for the first time can be a scary experience - and it can also be very expensive if not done correctly. This gives off the wrong impression where it is extremely complicated to invest internationally and because of this reason alone - many choose to stay within their comfort zones in Malaysia and choose not to invest internationally at all.

With the rise of technology and FinTechs in the recent year, investing internationally is no longer as difficult/expensive as it used to be (say, 10 years ago) hence more the reason we should look internationally to diversify our portfolios.

This article is written to help beginners understand various ways to get started with investing internationally - but before we get there, let's first understand why we should diversify internationally!

There are many good reasons why one should always look beyond just the domestic market - as the good ol' saying goes: "don't put all your egg in one basket".

Imagine if one day Malaysia becomes the next Zimbabwe and hyperinflation hits us and suddenly, all our years of hard work and our portfolio are essentially worth nothing now (okay, maybe a little too extreme, but you get the point)

Another factor is also that a significant chunk of our portfolio, through Employees Provident Fund (EPF), already has more than 70% exposed to local assets with only 30% international exposure.

Of course, this also depends on how long you've been in the workforce and whether if you're self-employed or wage earners, which will ultimately influence how much you've contributed thus far into your EPF fund. In my case, EPF makes up more than half of my total portfolio size and significantly affects my personal portfolio's investment decisions.

The next point is more relevant only if your style of investing is mostly passive than actively trading - which I'll further explain shortly in the next section.

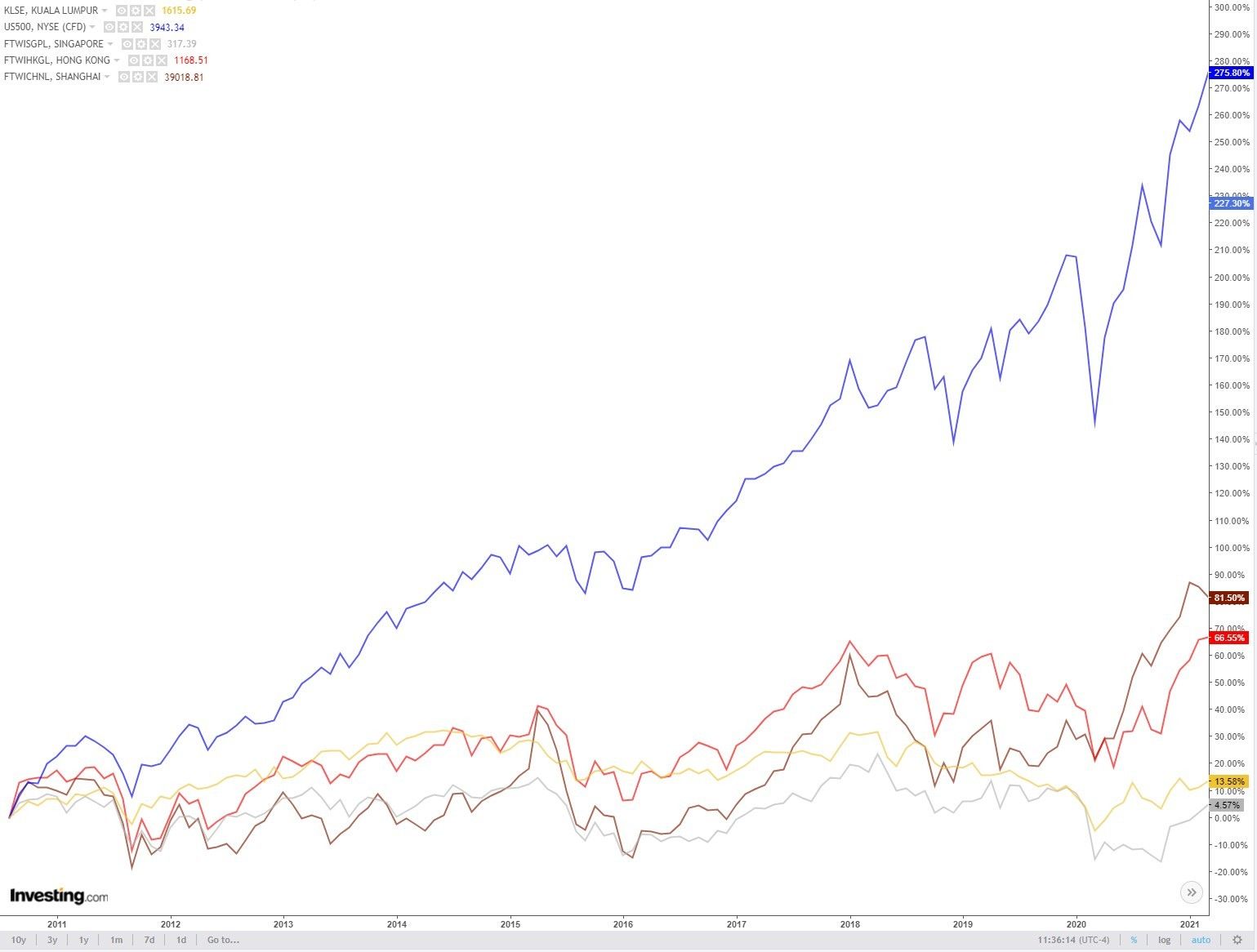

Long story short, if you're a passive investor like me, then there aren't many choices left in Malaysia for us to tap into (e.g. ETFs aka Exchange Traded Funds) whilst still allowing a good average yield considering that our market has mostly been stagnant for the past 10 years.

As you can see in the above comparison of indices; whilst the US, China or Hong Kong Index have been seeing tremendous gains over the last decade, the likes of Malaysia/Singapore indices have mostly been stagnant.

That's not to say that we should not invest locally at all - but merely the strategy employed might differ from those we deploy internationally.

Now that we know why one should always consider diversifying beyond Malaysia, there's another important concept that we must first understand before jumping into the 5 methods of investing internationally - and that is to first understand your own style of investing and find an investment strategy that works best for you.

While there has been a various form of investment strategies, they generally can be bucketed into two groups: passive investing or active investing. Both have their own merits and it is hard to argue which is better between the two - as what works for one investor may not work for the other so in the end it really depends on us as an individual.

Whilst this topic is not specific only to international investment, it is crucial to understand as most 'passive investing' generally works better in international markets like the US or China; compared to the Malaysia market which have very limited options (dividend or REIT stocks).

Passive investing is the investment strategy that takes a longer-term / macro-view approach in which the investor typically minimizes the number of trades performed. Some also call this strategy the buy-and-hold or buy-and-forget style.

As part of risk management for this strategy, investors will typically diversify into several asset classes, geographical coverage, or industries. One of the most popular passive-investing methods is to buy a low-cost index fund that tracks overall market movement, a.k.a. the "average" market performance regardless of the market cycle (bull run vs bear market).

This investment style is suitable for investors who may not be able to allocate enough time to study the market dynamics and prefer to just ride along with the market average returns. For this strategy to work effectively, investors must be able to separate their emotions from their investments, and always take the long-term view when it comes to investing.

Whilst you will never be able to "beat the market" with this approach, you will be able to simplify and automate your investment as much as possible and also save on fees due to the lower number of trades whilst still ensuring enough diversification.

Active investing is the investment strategy that tries to capitalise on the opportunities created by the market fluctuations and maximises the profit leveraging the market volatility. Some prefer to call this the beat-the-market or timing-the-market style.

Unlike its passive investing counterpart, active investing sits on the opposite end of the spectrum which encourages the investor to make trades more frequently, buying into different asset classes (usually stocks) and selling them at the best timing to maximise the gain - also known as buying low, selling high.

This investment style is suitable for investors who prefer a much more hands-on approach to do their thorough research before buying into the asset, maximising their potential returns in the shortest possible time before moving onto the next trade as an attempt to "beat the market".

As the investors will also have to ensure that they get it right than wrong most of the time, and also to limit their potential losses in the event their judgement was wrong. This means that investors have to spend more time managing their portfolio and also performing more trades, resulting in more commissions paid.

There's no hard and fast rule on which investment strategy is better as everyone have their own preferences. As an investor, it is important to find a style that works for you - something that helps you to sleep comfortably at night.

Having said that, most studies suggested that passive investing works better for the general population; and only a very selected few that employed an active investing strategy actually have beaten the market.

For example, I maintain more than half of my portfolio under the passive investment approach through various ETFs and long-term stocks considering my risk appetite and also the amount of time I can afford to follow the volatility and movements of the market.

I do employ active investing on a very small portion of my portfolio, but rather than trading the stocks actively in the short term (<3 months), it will be held at least for the mid-to-long term (6 months to 2 years).

Now that we have learnt about the reasons to invest internationally and also the different investing styles that may suit us - let's hop into the actual methods on how we can invest internationally as Malaysians.

These methods will be sorted from the most expensive to the most optimal/cost-effective option for the majority of us Malaysians. As always, pick one that is best suited for your personal circumstances.

Not too long ago before FinTech disrupted the entire finance industry, this used to be one of the two common approaches when it comes to investing internationally in foreign stocks (with the other being unit trust/mutual funds).

Most of our local brokerages (e.g. Maybank2u, HLeBroking, ...) allows the investor to opt for additional service to access the Foreign Shares Trading, granting investors access to some of the well-known international markets (e.g. US, Singapore or Hong Kong).

Depending on brokerage, most charge around 0.5% commissions with a minimum commission of around $30USD - some higher, some lower. To add salt to the wound, since the foreign currency will be managed by your brokerage, you will also be at their mercy when it comes to foreign exchange rate and/or additional fees (if any, such as deposit fees, foreign trading handling charges, dividing handling fees, etc.).

These reasons combined are why people have the general conception that "it is expensive to invest internationally into foreign shares". An investment of RM500 with this approach is simply not worth it, as more than 30% will be paid to your brokerage due to the minimum commissions amongst other fees. And we're only talking about 1 transaction here - imagine diversifying ?.

Having said that, one of the (few) key advantages of going this route is to always have peace of mind since these brokerages are always regulated by Securities Commissions Malaysia - and you only have to deal with your brokerage throughout the international investment process.

Given how expensive it can get to purchase multiple "individual stocks" through the above method, many of us opted to purchase unit trust/mutual funds which essentially is a financial product that holds a basket of stocks as its underlying asset.

When we say unit trusts / mutual funds, most in Malaysia will probably be thinking about the Public Mutual fund house. Indeed - they are one of the most commonly known fund houses but definitely not the only one. There's plenty of other fund houses such as Principal Asset Management, Affin-Hwang Asset Management, Kenanga Investors, Manulife Investment Management, etc.

Aside from fund house themselves, there are also "one-stop shops" such as FSMOne (by iFAST Capital) or eUnittrust (by Philip Mutual) which offers most of the funds from a variety of fund houses except for Public Mutual funds (due to their in-house exclusivity).

Through this method, investors will be able to look for funds which has objectives aligned to the investors' goal, such as investing in foreign-listed companies / foreign-listed technology companies / etc. Whilst cheaper than buying individual foreign stocks through local brokerages, it can still get expensive when we add up all the fees over the long run.

Depending on whether if investor purchases directly from the fund houses' agent which typically has upfront charges of at least 3.5% to 6%; or purchasing from one-stop shops which generally have negotiated lower fees with fund houses (and passing on the savings to the investors) with upfront charges of only 1% to 2%.

On top of that, there are usually annual management fees charged directly by the fund, costing investors at least 1% to 2% annually (depending on funds and fund houses). Like other options, these fund houses are always regulated by Securities Commissions Malaysia.

One of the hottest trends in automating investing in Malaysia today is through Robo-advisors - such as the likes of StashAway or Wahed. In layman term, Robo-"advisors" tries to understand your high-level investment philosophy, investment horizons, and risk appetite to propose a portfolio allocation that works for you.

As the involvements required from humans are further reduced/eliminated, they will then be able to charge lower management fees at approx. 0.8% per annum. Additionally, most Robo-advisors today will invest in low-cost ETFs which generally have 0.1% to 0.4% expense ratios and all these will add up to be below 0.9% - 1.3% in fees per annum. It is relatively cheaper when compared to the likes of unit trust which are mostly managed actively by portfolio managers with above 1.5% - 2% fees.

One of the key advantages for Robo-advisors is the flexibility on the contribution amount with flat %-based cost, regardless of how much you put in. This provides greater flexibility for investors to automate their investments even if the monthly contributions are low, without incurring expensive fees.

For example, when depositing with StashAway via MYR, they charge only 0.1% upfront cost (attributable to the foreign exchange fees) with the spot exchange rate to convert it into USD to buy several underlying ETFs - up to 6 or more depending on the portfolio. It is almost impossible to achieve this scale of upfront cost even when performing DIY ETFs by yourself unless you earn in recognised currencies such as SGD/HKD/USD which can be deposited directly into some of the foreign brokerage without involving foreign exchanges.

With the simplified approach and minimal involvements required from the investor (aside from depositing money), it helps to simplify their investment strategy and this can be an advantage or disadvantage depending on the type of investors. For example, with StashAway you basically won't be able to do the "active trading" style, unlike the other methods.

Read also: My StashAway Malaysia Review: Investments Automated

Through Bursa Malaysia, there are already 13 ETFs listed excluding leveraged & Inverse ETFs, and about 8 ETFs has exposures outside of Malaysia - mostly focused on China Fund, ASEAN Fund, US Titans, Asia ex. Japan, and GOLD Tracker which you can find the latest list on Bursa Malaysia's website.

With these ETFs listed in Bursa Malaysia, investors will then be able to buy the ETFs using their local brokerage account incurring standard local fees, which is relatively cheaper when compared to foreign trading through local brokers.

While the options for the investor to choose from are severely limited, they can be a good start for those who may have limited capital; or do not want to deal with hassles of international brokerage/fund transfer - provided that the listed fund aligns with the investment objective of the investor.

Due to its extremely low volume, the price can be quite volatile at times and mispriced at a premium or undervalued compared to its underlying stock value (NAV). This is one of the many reasons why most of us decided not to invest in ETFs through Bursa Malaysia and have since decided to DIY through international brokerages.

Similar to the other options earlier, these brokerages are always regulated by Securities Commissions Malaysia - and you only have to deal with your brokerage throughout the process without involving foreign exchanges since it is already managed at the ETFs fund level.

In a nutshell, rather than buying foreign listed stocks / ETFs through our local brokerage which charges a variety of fees, it's so much more cost-efficient to buy it directly through an international brokerage providing direct access to these markets resulting in lower fees.

What's a better way to reduce cost than through direct ownership of the respective stocks or ETFs?!? Whilst true to some extent, it really boils down to the investors' style as well as their capital.

For passive investors or buy-and-hold strategy with stocks / ETFs, a brokerage that provides low commissions with coverage to the US, London and HK will usually suffice - as it provides wide enough coverage for funds domiciled in different countries to maximise the tax efficiency - I'll detail this in my separate blog post.

As for active investors who may make several trades in and out to capitalise on the market volatility, then perhaps brokerage who offers zero commissions with only US coverage will be more than sufficient, as this avoids the stacking effect of fees for every trade that we take.

Nevertheless, regardless of style, the potential will only be maxed out if you have a huge amount of cash to deploy - as the cost goes down when you inject higher upfront capital, reducing the overall cost incurred to your portfolios.

Before you jump straight into the bandwagon of the International Brokerages, make sure to read the following chapter where I briefly describe the cost efficiency for passive investing internationally.

If you want to get started with this method, check out a few of my other articles where I wrote about this topic intensively: Beginner's Guide: Investing Abroad via Interactive Brokers from Malaysia and Journey on choosing the 'right' International Brokerage.

Do note that none of these international brokerages are regulated by Securities Commissions Malaysia - unless they decide to open up their physical branch here.

For any investment - cost efficiency matters. Period.

Depending on the cash amount that you have on hand, you may have to use a mixture of different investment methods spelt out above to achieve a "cost-efficient" investing.

Frankly, this topic is deep and can get very comprehensive technical just by itself, and I was initially planning to only write this on my separate post when comparing StashAway vs. DIY ETFs. But this important topic is often ignored by most so I decided to put this through together with this article earlier.

Fret not, what I'll do today is to at least summarise it in layman term with some calculations without going too crazy just to help you to grasp the concept of the entire cost of investments. For the comparison, I will be going in from the perspectives of a passive investor where the strategy is to minimize trades through a long-term approach.

In general, when it comes to buying international stocks / ETFs through your international brokerage, the key considerations are typically the:

This is why the investing strategy should always be personal depending on your investing style, capital, and time commitments.

Just to illustrate my point, if you invest only RM500 per month into 2 different ETF's via the "TradeStation Global / Interactive Brokers" route:

| Description | Cost ($USD) |

|---|---|

| Foreign Exchange Rates (Wise) | ~$2 |

| Currency Conversion (IBKR) | $2 (optional) |

| Trade Commissions (IBKR) - 2 ETF's | $1.5 x 2 = $3 |

| Annual Management Fee (IBKR) | n/a |

| Fund Expense Ratio (ETFs) | 0.1% ~ 0.4% |

|

TOTAL: |

One-Offs: $5 ~ $7 (~RM20.59 to ~RM28.83) |

Compare that with another scenario, say, we accumulate at least RM5000 over X months then "move" the funds to perform the same trade above.

The above calculation is obviously over-simplifying things - as we haven't factored in the cost of diversification yet (see how in the examples we're limiting to only 1 or 2 trades per funding).

Unless you are able to consistently fund more than RM5K towards your overseas brokerage on a monthly basis, StashAway might be a more cost-efficient method for you when it comes to automating monthly investments.

Using the same RM500 as an example, the cost to diversify into various ETFs will be so much more efficient through StashAway:

| Description | Cost (RM) |

|---|---|

| Foreign Exchange Rates (StashAway) | Spot Rate |

| Currency Conversion (StashAway) | ~0.1% = RM0.50 |

| Trade Commissions (StashAway) - usually above 6 ETF's | RM0 x 6 = RM0 |

| Annual Management Fee (StashAway) | 0.8% |

| Fund Expense Ratio (ETFs) | 0.1% ~ 0.4% |

|

TOTAL: |

One-Offs: RM0.50 |

Of course, the above comparison is overly simplified as we are only factoring in the one-time upfront cost when DIY-ing our ETF purchases. There are also other factors to consider such as the amount of diversification, portfolio rebalancing, as well as annual management charges from StashAway (which is non-existent for DIY ETFs)

I hope that you have learnt something today on why diversifying your portfolio internationally will help you in the long run. Always consider your personal circumstances to choose the most fitting option for you, and there's absolutely nothing wrong with mixing different styles or methods for your international investments!

One of the main driving factors behind your decision will likely be based upon your most optimal trade-sizes and duration required to accumulate enough funds to strive for maximum cost-efficiency when it comes to investing. I will be diving further into this topic in the future with more examples so stay tuned on my blog posts!

As always - thanks for reading and see you again in my next post! If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}