If you have read my story, you must have noticed that I have only restarted my financial journey sometime in late-2019.

At that point in time, I knew I had to do something before things got worse with me spiraling into further debts. Looking back now, I am so thankful that I forced myself to restart my budgeting habits because if I haven't, I'm pretty darn sure that I'll be in worse shape today, perhaps spiralling into even more debts!

Am I already perfect, and having mastered the Art of Delayed Gratification and Personal Finance in life? Nope, definitely not yet - with a long distance away from that! I still splurge occasionally, and immediately feel guilty about it. One thing's for sure though - my spending will still be below my means thanks to the taxation inflicted on myself 😛

Frankly speaking, I feel that I have been mostly playing the whack-a-mole game throughout 2020. At least the machine didn't break down this time...

I briefly wrote about it in my getting started guide towards financial freedom and will write a more detailed post in the future. But in a nutshell, I believe strongly in zero-based budgeting as it forces you, by discipline, to spend within your means. You simply cannot (or rather, shouldn't) go over budget because it will make the entire budget untrustworthy and defeat its purpose.

Upon receiving my net salary, I will always deduct at least 20% for savings/investments as a form of self-taxation by "paying-myself-first". I would then budget the remaining balance in three buckets:

The total amounts budgeted for all 3 buckets above shall not exceed the balance provided earlier, and I make it a habit to break down infrequent expenses into monthly budgets to help make things more predictable. This way, even if the expense finally hits me out of the blue - there'd be some spare floats which was funded from previous months' budget to help pay the bill, at least partially (e.g. car broke down; or angpao for friend's wedding dinner).

After reviewing my finances in late 2019 and throughout 2020, I noticed a bad habit of mine which happened again at the time when I'm writing this post - I tend to spend future money by leveraging 0% instalments.

With COVID-19, I had the luxury to work from home most of the time since March's lockdown (or MCO - Movement Control Order). This definitely have helped to provide me with a significant boost on my savings rate as I didn't need to spend much on meal or transportation.

When it comes to cooking - my mom does it best in her easy-and-lazy bland style and over the past few months, I think my taste buds have already adapted the bland taste. Nowadays even mild spicy or greasy food is enough to upset my stomach/digestion....

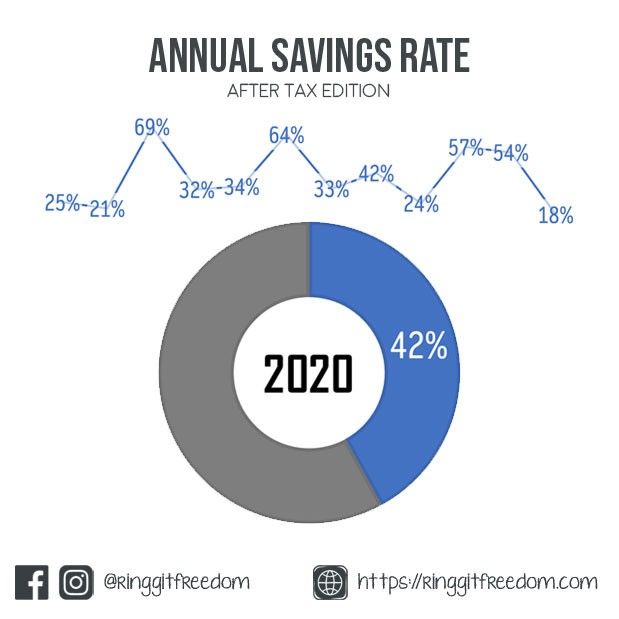

So far it seems like I'm able to maintain above 24% savings rate on a month-to-month basis except for December, due to the larger-than-expected "one-offs" - you can read more about it here.

I managed to hit 42% savings rate on an annual average wise for 2020, which was mostly contributed by windfalls / bonuses. The strict policy which I implemented last year where “every bit of extra income is strictly for savings/investments purposes” have definitely helped me.

The next biggest hurdle for me is whether if I can continue to “squeeze” out more savings by reducing my expenses. Frankly speaking, I find that to be really hard unless I take on a drastic approach to aggressively cut back on my lifestyle, which might even make my life not enjoyable at all. MCO obviously helped me to save on some essentials this but I ended up “redirecting” the funds and spent it on something else instead.

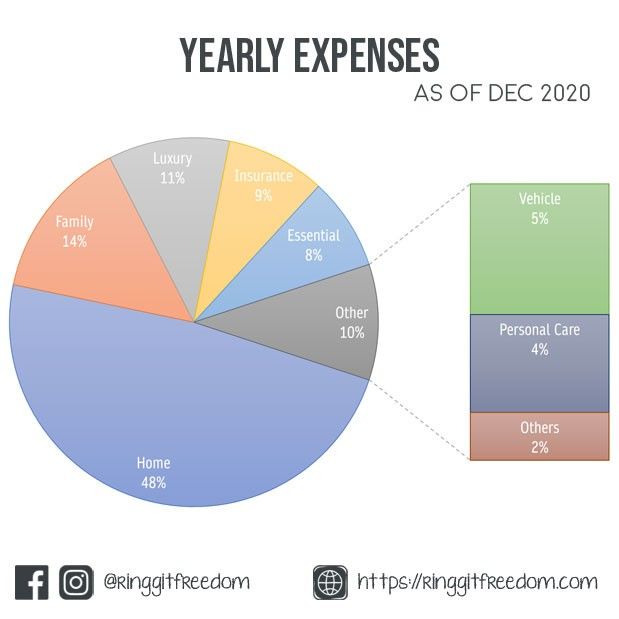

Taking a look at my top 5 largest spending categories in % vs. total expenses excluding Investments, most of it goes into home-related expenses followed by family, which would be difficult to adjust unless I decides to move out of my own place.

Whilst I definitely can better manage my 0% debts to minimise my spending of future money; I believe that the upside would be rather limited as compared to focusing on growing and diversify my active income sources.

No doubt the conscious and deliberate financial planning have helped me to amass my first 10K and recently having crossed my first 100K mark. Still the biggest contributor was the growth of my active income sources. Obviously I also learnt the hard way that higher income doesn't necessarily equate greater wealth - if no conscious efforts are put in place to curb lifestyle inflation from eating away the growth at a way faster pace.

Reflecting on my year so far, I am grateful to still have a strong career amidst the whole COVID-19 situation but I also have witnessed quite a number of layoffs within or outside my company. It's a scary survival game where the fittest may survive. And the easiest way to do so is to never stop learning and challenging my own growth.

Whilst upskilling myself have been proven fruitful and also rewarding so far, I believe it is also time to expand myself beyond "just my day job" and learn skills beyond my career paths. Maybe, just maybe, but this is to better prepare myself just in case if one day I decided to hop into the hot water and start my own company; or when opportunity comes for me to pick up bigger portfolio where wider perspective helps.

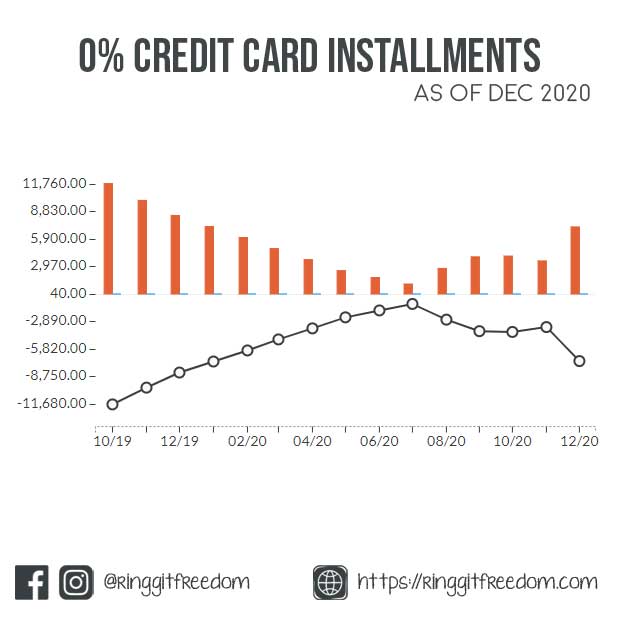

Back then, I didn't really kept track of my debts "burn-down chart" as I have been mostly focused on getting my finances back up on feet - by trying my best to respect THE BUDGET and keep my spending within its limit after the self-taxation, necessary expenses, and fun monies for my own pleasure

One thing I noticed over time was that quite a significant chunk of my monthly fixed expenses went towards paying down my 0% card instalments.

Whilst preparing for this post, I decided to retrospectively add some data points in my budget file to take a glimpse on my card leverage behaviours for the past years. Keeping things simple - I only went back to the first month I restarted my financial journey in Oct 2019.

Honestly, I am surprised at the effect that budgeting has on me. I started with more than RM12K debts and that aspiration and desperation to chase after "zero"-based budgeting have managed to put a pause into never-ending new instalments.... or at least until recently 🙁

Prior to budgeting, if my memory serves me right - I was signing up at least one new instalment of at least RM2k - RM3k every 2-3 months, which was deteriorating my financial health (and then I wondered where all my money went).

The budgeting habit helped me to realise that I was at my commitment limit and managed to breakaway from new instalment for at least 10 months

Frankly speaking - I still haven't found a method to completely break free from the temptations of 0% instalment. Like who doesn't like enjoying instant gratification with delayed payments!?

There were some significant dips again in late 2020, where I made additional purchases on 0% instalments in combinations of family, work, and mostly for leisure purposes.

Her eyesight was deteriorating and after spending YEARS convincing her (talking about stubborn... I got it from her too!), she's finally willing to go for eye checkup.

I didn't want to give her any chance to go back on her words, so I bought a branded quality frame with multi-focal lenses on the spot. Knowing her style (remember, she was the one that taught me basic finances/budgeting), she definitely won't let it go to waste and will continue wearing it 😀

Thanks to COVID-19 (and my kind company) I have been working from home almost full time since MCO started, except ~6 weeks where I had to work from the office when situations got better.

I used to have access to printers in office for works (and personal *cough*) usage whenever I needed to print something. But with the prolonged work-from-home situation it's just simply not possible for me to go to the office whenever I need something to be printed, and may not be appropriate especially if it is for personal usage.

So I finally decided to invest in one home-office printer and from my past experience and usage patterns, I decided to go for laser monotone with 3-in-1 functionality rather than inkjet as it tends to dry up overtime.

I consider it as my own guilty-pleasure. I've been wanting a TV in my bedroom for my occasional drama binge since I moved into my new home back in February last year.

But I managed to put off the thoughts and delayed my gratification for as long as I could, until I came across a deal that I couldn't resist as part of my partner-employee purchase program and I kinda went-ahead with the purchase, with long 0% payment terms.

I have no excuses for this. I failed badly in my delayed gratification and are still ashamed of myself. What happened to me walking the talk?!?

Unlike the TV which I managed to delay my gratification for more than 1.5 year; I barely lasted 7 days for this one.

And the funny part? I was researching on the eleventh hour to look for something I can buy (mobile phone, tablet or laptops) and claim the RM2.5K special tax relief for a quick profit, by reselling the device to others with a slight discount.

For some reason, it ended up with me falling victim to myself and bought a M1 Macbook Air after seeing its impressive fanless CPU performance. Mind you - this is coming from a life-long Apple hater. Yes, I hated Apple's product with a passion and swore to never buy any Apple products, except AAPL (stock). And look what happened...

I guess I can't fully blame myself - I've always been a geek and always had a soft spot for high mobility-productivity workhorse - the same reason I bought my Surface Pro 3 back in mid 2014. Maybe I can use this as an excuse to introduce my mom to the world of computer (she's a technology laggard :P)

Whilst these debts technically have 0% interest, I still want to aim to keep these debts as low as possible as it eats into invest-able portions and costs me more in the long run (spending vs. investing). Basically for every 0% instalment purchase made, I am spending monies from my future - money that I do not currently have yet.

Frankly speaking, I don't know if I will ever at all succeed to maintain ZERO outstanding 0% instalments, as economically it make senses at time for necessary purchases of big-ticket-items. Though by looking back at my past years spending behaviours, I realise that I really love gadgets. Whilst not as extreme as some of them whom changes new phone/laptop every year; but still hardcore enough compared to most others.

One way that I'll try moving forward is to allocate and budget these amounts upfront by breaking down my gratification monies into affordable monthly budgets where I can accumulate and spend without guilt once the jar is full, which may help reducing my reliance on spending future money.

Even if I have budgeted enough of my gratification monies into a pool, I don't see myself completely stopping zero 0% instalments as I believe this is one of a creative way to manage cash-flow when applied correctly. Think of it as such:

Only problem is that I must really have a self-discipline to avoid what happened in Q4 2020. Like it or not, I have to force changes on myself to become a better version than yesterday. Let's see in 2021's year end review...

There's always these "if I had known..." feeling and I just have to consciously remind myself to focus on moving forward onto the future. While still far from being perfect, this has to be one of my proudest and productive year when it comes to investing.

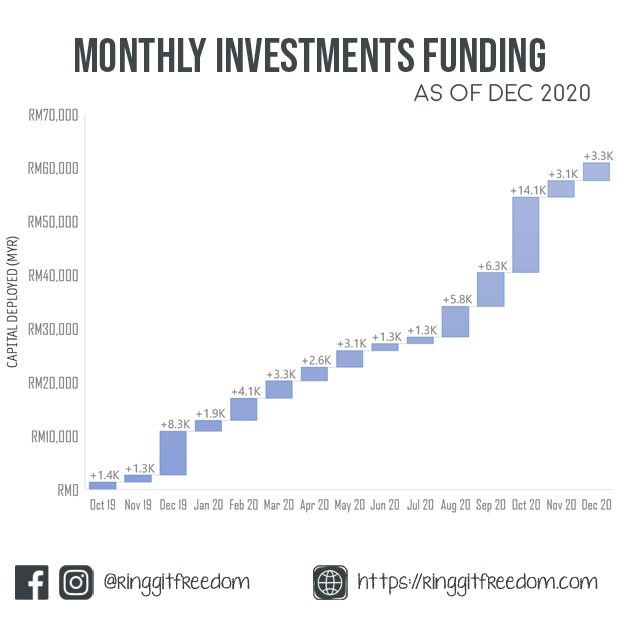

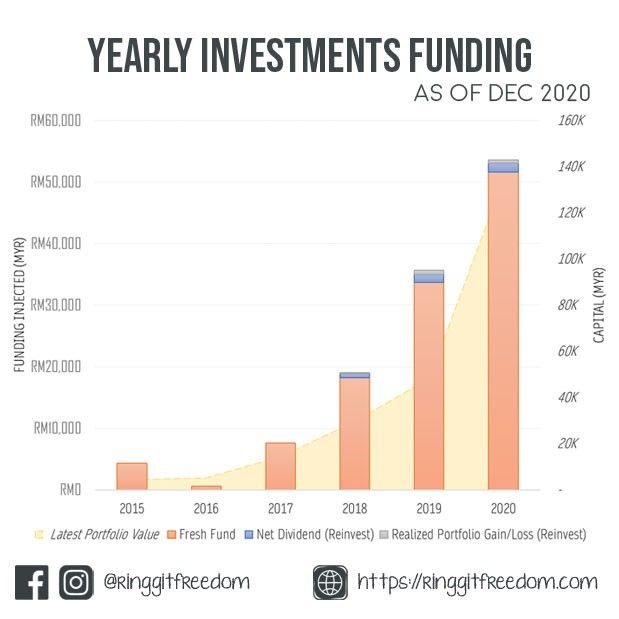

Unlike the past few years where I will only invest when I have spare changes, which only happens by chance. Throughout 2020, investing is part of my budgeting where I have to invest the moment I receive my paycheck (taxing myself first) and hence it happening by design. I do this mostly through my scheduled direct debits of StashAway, alongside with periodical stock purchases in both local market and international market.

I managed to double my personal portfolio size from approximately RM69.3K in 2019 to RM134.5K in 2020, thanks to the aggressive savings and consistent investing throughout the year. Combined with my EPF and Cash, I'm finally sitting at -RM26K Net Worth and are one step closer to my goal of "Zero" Net Worth!

One biggest regret I have was not to get my shit together earlier. If I've done that perhaps I would already have a bigger pile of cash to be deployed during March's crash but instead most of my savings went into building my emergency fund (I had zero emergency fund until March 2020 and that's when reality sinks in :D). I guess the most important thing is that I have started holding myself accountable to my own financial journey.

Despite the drawbacks, 2020 is still one of the very few years that I took a more serious / proactive approach in managing my portfolio and assessing them holistically from all angles. I basically have exited several of my unit trust portfolios and mirroring the diversification into a more cost-efficient approach via direct holdings of ETF and Stocks through my international brokerage. I have also decided to start divesting part of my EPF funds via i-Invest to mainly diversify further beyond Malaysia due to my significant over exposures of Malaysia market.

I hated writing new year resolutions as it feels bad when I failed in achieving them - but I'd like to try it for a change.

2020 have really been a unique year for me. As an introvert myself, I always enjoyed the presence at home but never imagined that I'll also be affected by cabin fever being locked in my room for too long :P.

Whilst it is definitely not a best year with the pandemic and all, still from financial perspectives, I am mostly happy that my commitment helped me to put me back on track where I left of previously. Whilst not perfect, it is still on the right track and every successes, no matter big or small, shall be celebrated! ^^

After all, I am still learning and also have my own flaws and downsides. Temptations are hard to control - and as much as I consciously reminds myself to delay my gratifications, sometimes I just end up losing it. I guess I just need to do my best on the saving up a "guilt-free piggy-bank" part for some of these impromptu expenses and have a better self-control on my "wants".

Nothing alarming yet honestly as long as stick with my mandatory-self-tax principle, they'll all be under control. I hope that 2021 will be a better year with my plan to increase my forced self-taxation rate contributing into my savings or investments.

As always, see you in my next post! If you haven't already, be sure to follow me on my Instagram, Facebook and YouTube for latest updates!

Cheers,

Gracie